Dropping your health insurance? Here’s how to pay for healthcare in 2026

Costs happen. And price increases on everything could be the most life-impacting development of 2025. Looking ahead, millions of people are expected to decide that health insurance is unaffordable for them in 2026 — and they’ll likely cancel their health coverage.

But health insurance is not the only way to pay for healthcare. Many people are uninsured and face healthcare costs out of pocket. They are known as cash-pay customers. This option can be daunting for people with serious conditions such as cancer, but there are ways to successfully navigate costs without health insurance while avoiding medical debt.

GoodRx, a platform for medication savings, shares how you can handle your healthcare costs if you drop your insurance for the 2026 coverage year.

Key takeaways:

- For the 2026 coverage year, every health insurance option available to you may be unaffordable.

- Whether you typically have a health plan or your coverage is sporadic — but you had health insurance in 2025 — you may opt to become a cash-pay healthcare consumer in 2026.

- If you can’t afford insurance or decide to go without a plan for 2026, you have many healthcare options.

What are your options for healthcare without insurance?

In the U.S., most people have health insurance. This coverage comes through Medicaid, Medicare, or individual and family plans offered by employers. In 2025, more than 24 million people were covered by a plan offered on the Affordable Care Act (ACA) marketplace. But enrollment is expected to plummet if the income-based ACA premium subsidies (also known as premium tax credits) aren’t continued at the same levels in 2026. These subsidies are what made plans affordable for about 22 million people in 2025.

Healthcare options that don’t involve insurance

If you can’t afford health insurance in 2026 — or you’ve decided to drop coverage for any reason — here are some self-pay healthcare options you might use.

- Direct primary care: Direct primary care (DPC) is an alternative healthcare model for accessing medical care without insurance. You make the care and payment arrangements with a healthcare professional and pay out of pocket. DPC may be offered by a physician, a physician associate (PA, also known as a physician assistant), or an advanced practice nurse, such as a nurse practitioner. Your DPC arrangement typically covers routine care, management of chronic conditions, acute-care visits, and care coordination. Emergency and hospital services aren’t included.

- Cash-pay care with a good faith estimate: If you’re not using insurance to pay for your care, you are entitled to a good faith estimate (GFE), which is an itemized list of expected costs for a scheduled service. If your bill is $400 or higher than the GFE, you can dispute the bill.

- Concierge care: Concierge care is a membership-based model, often with an annual retainer fee that gives you direct access to a physician. Same-day appointments are usually available. Concierge care offices usually limit the number of patients and offer longer appointments than a typical practice. Concierge care often attracts higher-income consumers and may also be called concierge medicine, retainer-based medicine, a platinum practice, or boutique medicine.

- Medical cost-sharing: Sometimes called healthcare sharing plans, medical cost-sharing programs are communal models where group members pool their money to collectively cover everyone’s approved medical costs. Medical cost-sharing programs are not insurance and member costs may not be paid. There are financial risks and members can end up with unpaid bills, leading to hefty medical debt.

- Saving your premiums to pay for care: Many people have been paying hundreds of dollars monthly for health insurance premiums. What if, just for 2026, you redirected that cash to a savings account and used the funds to pay directly for healthcare? Healthcare facilities and hospital systems are signaling that more people are cash-pay customers. Increasingly, patient forms and healthcare professional search tools are offering specific guidance for self-pay and uninsured consumers.

- Tax-advantaged healthcare accounts: Your workplace may offer a health reimbursement arrangement (HRA) in lieu of health insurance. (You can also have an HRA with health insurance or use the funds to pay premiums for a plan you acquire yourself.) Only your employer contributes to an HRA. You typically don’t have to pay state or federal taxes on the money reimbursed to you from the account for qualified healthcare expenses. If offered by your employer, you can also have a flexible spending account (FSA) without enrollment in a health plan.

- Cash care: There are healthcare facilities and other convenience locations that have transparent and/or flat-free pricing for services, such as retail clinics — often found in pharmacies or grocery stores — and urgent care centers.

- Sliding-scale care: Care at community clinics is typically low cost, but not free. There are also free and low-cost healthcare options available nationwide.

- Patient assistance programs: If you don’t have insurance, you can qualify for free healthcare and prescription medications from patient assistance programs.

- Charity care: Also known as indigent care, you may qualify if you are medically indigent. This means medical bills make up a significant share of your income and medical debt threatens your financial stability. You’re financially indigent when you’re uninsured or underinsured and your household income falls below a certain threshold. Nonprofit hospitals are legally required to offer this type of financial assistance and some for-profit hospitals do too.

What about the ACA premium subsidies?

As of Dec. 5, 2025, ACA premium subsidies have not been approved for the 2026 coverage year. The question about whether these premium tax credits will continue has greatly impacted the open enrollment season. Even though the 43-day federal government shutdown ended on Nov. 12, 2025, the White House and Congress continue to negotiate about these healthcare subsidies.

Without the subsidies, premiums are expected to double, on average, in 2026. If they disappear, that means people with ACA plans must cover the full rate for their insurance. Many people who depend on these discounts to afford health plans have not enrolled in plans or renewed coverage for 2026 on the federal and state marketplaces.

In addition, premiums are spiking in 2026 for Medicare Part B as well as for many Medicare Advantage and employer-based plans.

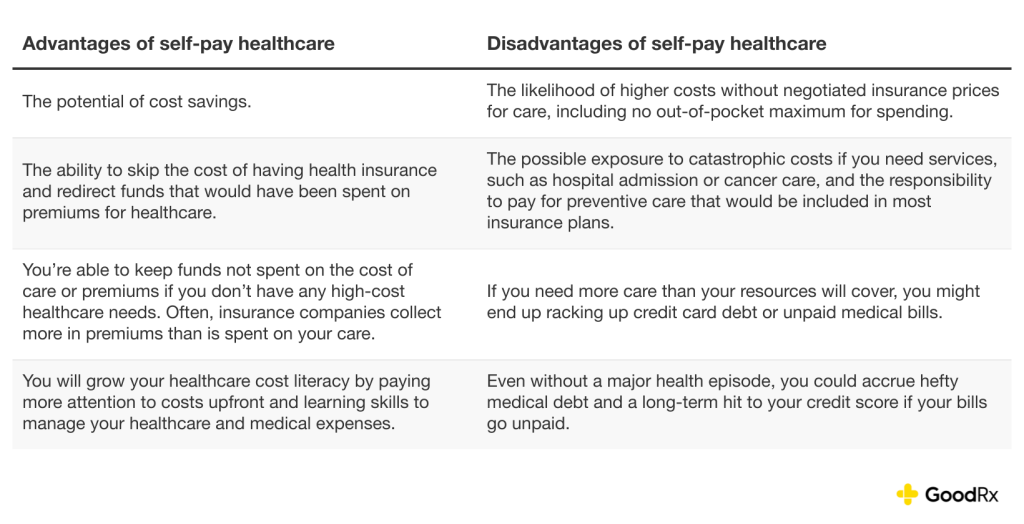

Pros and cons of self-pay healthcare

There are advantages and disadvantages of self-pay healthcare. It can be less costly, but not always. If you have even moderate health concerns, it is rarely less costly — especially if you develop an unexpected health issue. Before deciding to go this route, you may also want to consider options for accessing healthcare without insurance, such as:

- Cash-pay facilities near you.

- Having a strategy for comparing costs.

- Having the resources to pay for the healthcare — including prescriptions — that you or your family members may need while weighing the reality that not having insurance can expose you to massive medical debt.

Here’s a snapshot of some positive aspects of skipping insurance versus why dropping coverage might not be a good idea for you and your family.

Pros and cons of self-pay healthcare

Who might be able to risk going uninsured?

Lacking insurance has risks, including medical debt — which can lead you to medical bankruptcy. But being uninsured is also common. In 2023, an estimated 8% of the total U.S. population did not have insurance and more than 9% of people ages 0 to 64 were uninsured.

It’s important to note that choosing a year or more of cash-pay care is not ideal for most people. Those who might risk the least by choosing self-pay healthcare include:

- Healthy people who don’t have chronic conditions.

- Young people.

- People who are not prone to accidents.

- People with higher incomes.

- People who plan to sign up for insurance the following year (or sooner).

Why would you want to drop your health insurance?

Often, people don’t want to drop health insurance, but circumstances — chiefly cost — are why they can no longer continue with a plan. Reasons why you may want to drop your health insurance include one or more of the following:

- Premiums are unaffordable.

- The deductible is too costly for your budget.

- ACA subsidies might not be offered in 2026.

- The coverage does not meet your needs.

- The prescription coverage does not include the medications you take.

- You have access to another health plan that meets your needs and/or costs less.

- You move out of the coverage area.

How to cancel health insurance

You can cancel your health insurance by contacting your plan or if you (or your employer) are no longer paying premiums. Here’s how to cancel your coverage:

- Determine whether you are stopping coverage just for yourself or for everyone covered by your plan. This is especially important if you are canceling COBRA health insurance.

- Determine what coverage you want to stop. You may want to drop a comprehensive healthcare plan, prescription coverage only, dental coverage only, or just a vision plan.

- Determine whether you can cancel coverage. If you have an employee or group plan, you typically need to have a qualifying life event (QLE) or leave your employment to cancel coverage. If you have a Medicare Advantage plan, you can drop coverage during the Medicare open enrollment period, the Medicare Advantage open enrollment period, or if you qualify for a special enrollment period (SEP). You can disenroll from a standalone Medicare Part D plan during Medicare open enrollment, if you have a standalone Part D plan and a Medicare Advantage plan, or if you qualify for an SEP.

- If you have an ACA marketplace plan, you can contact the national or state marketplace that provided your plan — or the insurance company. You can also log into your marketplace account and cancel.

- A health insurance plan can be canceled by the insurance company if you fail to pay the premium.

- If you don’t sign up for health insurance during your open enrollment period — or take whatever action signals you want to drop your insurance for 2026 — you will cancel your coverage.

Is there a penalty for canceling health insurance?

A nationwide mandate set after the ACA law passed in 2010 was eliminated in 2019. You could face a requirement (some with a financial penalty) for not having health insurance if you live in certain states or Washington, D.C.

- California: Residents have a penalty for not having coverage, but the amount varies annually. For the 2024 tax year, the penalty was at least $900 per adult and $450 per dependent under 18 in a household. (This is the most current information available at the time of publication.) Residents can use the state’s Individual Shared Responsibility Penalty Estimator to determine the potential amount owed for the current tax year.

- Massachusetts: The Massachusetts healthcare individual mandate doesn’t apply to anyone under the age of 18. It also doesn’t apply to people with a qualified hardship or an exemption and those whose incomes are equal to or less than 150% of the federal poverty level (FPL). The penalty is assessed on a sliding scale. For instance, for the 2025 tax year, individuals without insurance must pay $300 per year if they earn 150.1% to 200% of the FPL and $588 per year if they earn 200.1% to 250% of the FPL.

- New Jersey: The New Jersey Shared Responsibility Requirement is assessed based on how many months people in the household did not have minimum essential coverage or a coverage exemption. For the 2025 tax year, the amount ranges from $695 to $4,908 for an individual taxpayer and increases based on the number of additional uninsured people in the household as well as household income.

- Rhode Island: The RI Health Insurance Mandate is whichever of these amounts is greater: 2.5% of annual household income or $695 per adult and $347.50 per dependent under 18.

- Washington, D.C.: The Individual Responsibility Requirement for anyone who goes without coverage for all of 2025 is the greater of: 2.5% of annual household income over the federal tax filing threshold or $795 per adult and $397.50 per dependent under 18, with a cap of $2,385 per family.

- Vermont: There is no financial penalty, but residents must report whether they have health insurance when they file their state taxes.

- Maryland: Residents are asked about health insurance status when they file state taxes as an avenue to enrollment.

The bottom line

Health insurance is not the only way to cover healthcare costs. People who access healthcare without insurance are known as cash-pay customers. This can be a tricky option for people with chronic conditions or very costly care, such as for cancer. But there are ways to successfully handle the costs of healthcare without insurance while sidestepping hefty medical debt.

Options used alone or in combination include: direct primary care, cash clinics, tax-advantaged healthcare accounts, sliding-scale care, patient assistance programs, and hospital charity care. Many people will decide whether to cancel health insurance in 2026 based on whether the Affordable Care Act (ACA) marketplaces have premium subsidies available.

This story was produced by GoodRx and reviewed and distributed by Stacker.