Gap insurance: Is it needed when buying a new car?

There’s nothing quite like the feeling of driving a brand-new car off the lot. The spotless interior, the gleaming paint, the distinctive “new car smell”—it’s a moment of pure excitement. You have signed the papers, secured the loan, and your vehicle is covered by your essential car insurance policy, which includes collision and comprehensive coverage.

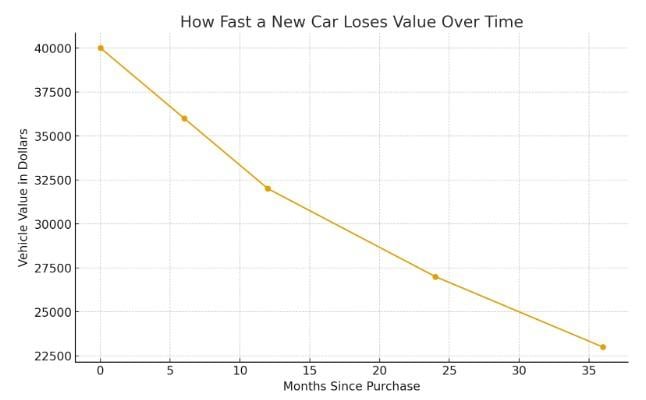

But here’s the brutal reality check your finance manager may have casually alluded to: depreciation. The instant those brand-new tires hit the pavement, that vehicle’s value takes a serious nosedive. Most vehicles depreciate by 20% or more in their very first year on the road.

Here’s where the important difference is: Your regular auto insurance, even with a “full coverage” including collision and comprehensive, only pays out an amount up to the vehicle’s actual cash value (ACV) at the time of a total loss. This is not the same thing as the purchase price or the amount you owe the bank.

That is no minor fluctuation, but rather a financial gap that could seriously expose you in case the worst happens. This is where gap insurance or guaranteed asset protection comes in, playing the vital role of the wallet’s safety net. Before you delve deep into quotes, Cheap Insurance explains what you need to know about gap insurance.

What is Gap Insurance? (And Why Does It Matter?)

To understand gap insurance, you first have to understand the gap it covers, which is a common issue when securing a loan for an expensive asset like a new car.

The Anatomy of the Gap

When you finance a new car, you owe the lender a specific loan balance. If your car is declared a total loss (due to a covered event like an accident or theft), your standard auto insurance policy with comprehensive or collision coverage pays out an amount based on the vehicle’s ACV. The ACV is the fair market value of the vehicle just before the incident.

Because of rapid depreciation, this ACV is almost always lower than your outstanding loan balance. Your insurance company will only reimburse you for the ACV.

Example Scenario:

- Day one: You buy a new SUV for $40,000, financing the full amount.

- Month six: You are involved in an accident, and the car is totaled. Your loan balance is still $38,000.

- The problem: Due to depreciation, your insurance company determines the ACV is only $32,000.

In this scenario, your auto insurance company writes you a settlement check for $32,000. You still owe the bank $38,000. That leaves you with a $6,000 shortfall that you must pay out of pocket for a car you no longer own. That is the gap.

Gap insurance is designed to cover this specific, painful difference. It settles the remaining loan balance, ensuring you do not walk away from a totaled car with nothing but a huge debt.

The following chart was created by CheapInsurance.com based on statistical data from Kelley Blue Book, LendingTree, and AutoNation.

The Decision Matrix: When Gap Insurance is a Near-Must

While it is a smart consideration for nearly all new car buyers, there are specific situations where Gap Insurance moves from “nice to have” to “absolutely necessary.” These situations are often tied to how your required collision and comprehensive car insurance policies operate after a total loss.

1. High Loan-to-Value (LTV) Ratio

This is the number one indicator. If your loan amount is close to or even exceeds the car’s actual value, you have a high loan-to-value ratio (LTV). A high LTV means your standard car insurance payout after a total loss will likely be insufficient to clear your debt. This usually happens if you:

- Make a small or no down payment. If you only put down 5% or less, you immediately start upside down on the loan (meaning you owe more than the car is worth). Your comprehensive and collision coverage will pay the actual cash value, leaving you with a huge loan balance that gap insurance must cover.

- Finance for a long term: Loans of 60, 72, or even 84 months (five, six, or seven years) mean you are paying down the principal more slowly, allowing depreciation to outpace your payments for a longer time. This prolongs the period in which a standard car insurance claim would leave you in debt.

- Roll Over negative equity: If you traded in your old car and rolled the remaining balance of that loan into your new car loan, you are starting with a significant gap on day one. This instantly makes gap coverage a requirement to prevent a double debt burden if the new car is totaled.

2. Rapid Depreciation Models and the Deductible Trap

Some cars simply lose value faster than others. If you have purchased a luxury vehicle or a model with a historically poor resale value, the gap between your loan and its actual cash value will grow faster.

This depreciation risk is compounded by your car insurance deductible. When your primary insurer (using your collision or comprehensive policy) pays out the actual cash value, they first subtract your deductible (often $500 or $1,000). The gap insurance then has to cover the remaining debt plus that deductible amount (though not all gap policies cover the deductible, so always confirm this detail). Without gap coverage, you not only pay the outstanding loan balance but also lose your deductible amount.

3. Extended Payment Deferrals or Leases

- Payment deferrals: If your loan includes a period of deferred payments (e.g., “no payments for 90 days”), the principal balance is not being touched, while depreciation is still in full swing. This is a massive risk period where your full coverage car insurance payout will almost certainly fall short.

- Leases: If you lease a vehicle, gap insurance is typically required. The leasing company is the true owner and mandates this coverage to protect its asset. It is often already included in your lease payment, but you must ensure it is present. This lease gap coverage functions exactly like loan gap coverage, protecting the leaseholder from owing massive termination fees if the car is declared a total loss by their comprehensive or collision policy.

How to Get Gap Insurance

The good news is that acquiring gap insurance coverage is generally straightforward; the prudent buyer’s goal is to secure the policy without incurring excessive costs. Price comparisons across providers are essential for a favorable outcome.

Option 1: The Dealership Finance Office

The most common place where gap insurance is offered is within the finance and insurance (F&I) office at the automobile dealership.

- Convenience: The process is easy, often presented as a single line item added directly to the car loan. This allows for immediate coverage upon driving the new vehicle off the lot.

- Cost: Dealerships frequently mark up the price of gap insurance significantly, often charging a flat fee ranging from $400 to $700. The premium is typically rolled into the total car loan, which means the borrower pays interest on the insurance premium for the entire term of the loan, increasing the final cost.

Option 2: The Primary Auto Insurance Company

Many major car insurance carriers offer gap coverage as an endorsement or rider to a customer’s existing comprehensive and collision insurance policy.

- Cost savings: This is often the most cost-effective option. When bundled with a standard auto insurance policy, the average annual cost of gap insurance is between $20 and $100 per year. Since the premium is paid yearly, it is not subject to the interest charges of the auto loan.

- Requirements and availability: Full coverage car insurance, including both collision and comprehensive, is required to add this endorsement. Policy availability can vary by carrier and state regulation, requiring a specific request to an insurance agent.

Option 3: The Lending Institution

The financial institution that provides the auto loan, such as a bank or credit union, may also offer a gap insurance policy.

- Competitive pricing: These rates are usually more competitive than those offered by the dealership, often providing a middle ground in pricing.

- Process: Acquisition requires an extra step in the financing process, as the policy is separate from the dealership’s transaction and the vehicle owner’s primary auto insurance coverage.

The Final Verdict

Gap insurance is not legally required, but for a new car buyer who secures an auto loan, it represents a fundamental piece of financial protection within a complete car insurance portfolio.

Consider this: For a minimal annual auto insurance premium, a vehicle owner secures coverage against facing a catastrophic accident that results in an empty garage and a massive outstanding car loan balance.

Key Action Items for the Smart Car Insurance Buyer

- Calculate loan to value (LTV): If the down payment is less than 20% or the auto loan term extends beyond 60 months, the gap risk is high, necessitating this specific type of car insurance.

- Shop around: Never purchase guaranteed asset protection from the dealership without first getting a quote from the vehicle owner’s current primary auto insurance carrier.

- Understand the car insurance policy: Ensure the gap insurance policy covers the primary insurance deductible. Verification of this detail is always recommended.

- When to cancel coverage: Once the car loan balance drops below the vehicle’s market value, which typically happens a few years into the loan term, the owner can cancel the policy and realize savings on their car insurance costs.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.