How your credit score really affects your car insurance rate

CheapInsurance.com examines how an applicant’s financial profile intersects with their driving profile in determining auto insurance rates. Most drivers know that factors like driving record, vehicle type, and residential ZIP code influence an auto policy. However, the credit-based insurance score often plays a significant role as well. This article explains the relationship between credit and insurance, outlines scenarios where credit matters least, and highlights crucial consumer considerations. Readers can also learn more about their car insurance choices.

What Insurers Mean by a Credit-Based Insurance Score

Insurers typically use a specialized score, often called a credit-based insurance score, instead of a standard FICO credit score. According to the National Association of Insurance Commissioners (NAIC), the factors used to calculate this score include:

- Payment history

- Outstanding debt

- Length of credit history

- New credit

- Credit mix

While often correlated with credit scores used by lenders, an insurance score is calibrated differently and is treated as just one of many factors in the underwriting process.

How Much Can Your Credit Profile Influence Your Auto Insurance Premium

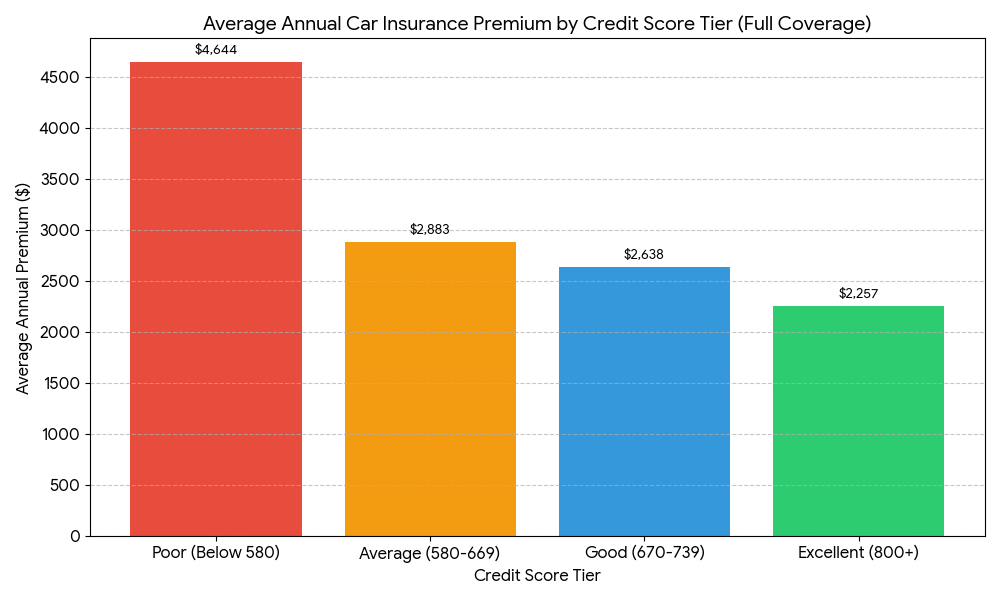

Research demonstrates that in many states, drivers with poor credit profiles pay substantially more for coverage than those with excellent credit profiles. For example, aggregate data from 2023 indicates that individuals with excellent credit profiles paid around $1,947 on average, while those with very poor profiles paid approximately $4,145.

Here are the typical impacts of credit on insurance pricing.

- Premium Increase: A drop of one credit tier may raise an insurance premium by 17% or more.

- Legal Use: Insurers in most states can legally use credit scores as a pricing factor when determining a driver’s risk.

- Variability: The degree of premium increase varies significantly by state and insurer; in some cases, the difference in annual cost is more than double.

Which States Prohibit or Limit Credit Score Use in Auto Insurance

Because insurance regulation is state-based, the use of credit scoring varies significantly across the country. Key rules governing this practice include the following.

- Total Bans: Four states (California, Hawai’i, Massachusetts, and Michigan) have banned insurers from using credit information to set auto insurance rates in most cases.

- Partial Restrictions: Additional states, such as Maryland, Oregon, and Utah, do not ban the practice entirely but restrict how credit information can be used. For instance, it may not be used as the sole reason to cancel or deny a policy.

- Regulatory Guidance: State regulators often caution consumers to check directly with their state’s insurance department because legislation in this area continues to evolve.

Why Credit History Matters for Auto Insurance Pricing

Insurers utilize credit-based insurance scores primarily for three reasons:

- Risk Proxy: Insurers view a strong credit history as a proxy for lower overall risk, associating more consistent payments and fewer financial stressors with historically fewer claims.

- Improved Risk Differentiation: Credit-based insurance scores allow insurers to incorporate nondriving behavior risk factors into pricing models, which significantly improves risk differentiation and, subsequently, profitability.

- Algorithmic Pricing: Because auto insurance is priced based on risk classes, many insurers integrate credit scoring as a key component of the pricing algorithm, alongside driver history, vehicle type, location, and other rating factors.

What You Can Do if Your Credit Profile Is Weak

In states where credit scores are permitted as a rating factor, drivers can take the following steps to help mitigate their impact on premium costs:

- Regular Monitoring and Correction: Insurers use a score tied to the consumer’s credit file, so inaccuracies matter. It is essential to monitor credit reports regularly and dispute any errors immediately.

- Improve Financial History: Improve payment history by staying current on all bills and keeping revolving debt levels low. These habits are key components for an insurance-friendly score.

- Compare Insurer Practices: Shop for insurers whose underwriting practices place less emphasis on credit scores. This is especially relevant in states where credit use is restricted or banned.

- Inquire About Other Factors: Ask an insurer or agent what other factors are weighted heavily in the state, such as driving record or vehicle safety features, so those areas can be strengthened.

- Geographic Advantage: Drivers who move to, or live in, a state where credit scores are not allowed as a rating factor will benefit from this legal protection.

The chart below is based on data from Experian and statistics from the National Association of Insurance Commissioners.

How To Interpret Your Policy and Ask Good Questions

When reviewing an auto policy or quote, informed questions can improve transparency and control costs.

- “Does the insurer use a credit-based insurance score in pricing for this state?”

- “When credit is used, what portion of the rating algorithm is because of credit?”

- “If credit improves or deteriorates, will that affect the renewal premium or just new business?”

An individual’s credit profile can matter significantly for automobile insurance coverage in many states, yet the rules are far from uniform. Knowing the state’s regulations, understanding how credit-based insurance scores are applied, and taking concrete steps to improve or mitigate credit impact are beneficial for managing policy costs.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.