Should you choose a high-deductible health plan? What to know about the pros and cons

With the enhanced Affordable Care Act (ACA) premium tax credits set to expire soon, many people could see their marketplace plan premiums rise in 2026. As a result, some may consider switching to a high-deductible health plan (HDHP) to keep monthly costs manageable.

An HDHP keeps your monthly premiums low while typically providing 100% coverage for in-network preventive services before you meet your deductible. Sounds good, right? But it’s not quite that simple.

An HDHP can save you money up front, but it also comes with higher out-of-pocket costs if you need medical care beyond routine checkups. In this guide, GoodRx explains how this type of plan works to help you decide whether an HDHP is the right fit for your budget and healthcare needs.

Key takeaways:

- A high-deductible health plan (HDHP) is a health insurance policy that has a lower monthly premium and a higher deductible.

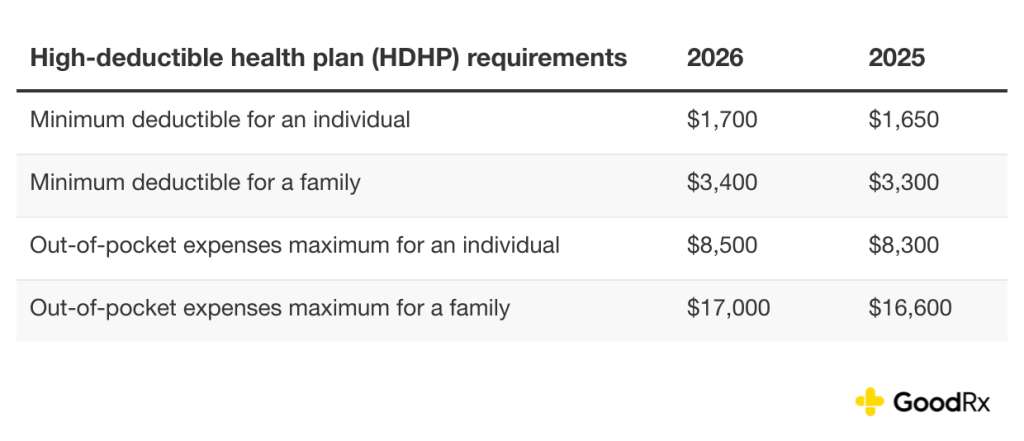

- The federal government defines the deductible amounts for plans to qualify as HDHPs. For 2026, the minimum deductible for an HDHP is $1,700 for individuals and $3,400 for families.

- HDHPs typically cover all preventive, in-network care in full, even before the deductible is met. Other types of medical services are only covered once the full deductible is paid.

- Because of recent policy changes, many HDHPs can cover telehealth visits before the deductible is met without affecting health savings account (HSA) eligibility. Starting in 2026, bronze and catastrophic Affordable Care Act (ACA) marketplace plans will qualify as HSA-eligible HDHPs.

What is a high-deductible health plan (HDHP)?

An HDHP is a health insurance plan with a high deductible and, typically, lower monthly premiums compared to a traditional health insurance plan. A health plan deductible is the amount you pay out of pocket for medical care before your insurance covers any costs. A premium is what you pay every month for your plan.

More specifically, an HDHP is a plan with a deductible that meets or exceeds the minimum annual amount set by the federal government.

What is considered a high-deductible health plan in 2026?

To qualify as an HDHP in 2026, a plan must have a deductible of at least $1,700 for individual coverage or $3,400 for family coverage. These plans also have out-of-pocket spending maximums, which include coinsurance, copays, and deductibles, but not premiums. In 2026, spending is capped at $8,500 for an individual and $17,000 for a family.

If you reach your out-of-pocket maximum, your plan will pick up 100% of your costs for the rest of the calendar year. But keep in mind that the limit does not apply to services outside your network.

The table below shows HDHP minimum deductibles and maximum out-of-pocket expenses for 2025 and 2026.

What does a high-deductible health plan cover?

If you’re enrolled in an HDHP, your in-network preventive care is covered without you having to pay the deductible first. Because of this, a high-deductible plan can be a smart financial decision.

An HDHP may also cover some telehealth or virtual care visits before you meet your deductible. Under the One Big Beautiful Bill Act (OBBBA), a permanent safe harbor lets plans do this without affecting enrollees’ health savings account (HSA) eligibility. This rule applies to plan years beginning after Dec. 31, 2024.

A list of preventive services and screenings covered by HDHPs is available at Healthcare.gov. Here are some examples of medical care that may be covered in full before you meet your deductible.

Adults

All marketplace plans and many other plans must cover the following preventive services for adults:

- Screening for abdominal aortic aneurysm (bulging of the main artery in the belly) in men of certain ages who have ever smoked.

- Aspirin to prevent heart disease for adults of certain ages.

- Blood pressure screening.

- Cholesterol screening for adults based on age and risk factors.

- Colorectal cancer screening for adults ages 45 to 75.

- Depression screening.

- Type 2 diabetes screening for adults who qualify based on age and risk factors.

- Certain immunizations, such as the flu shot.

Women

Here are some preventive services that must be covered for women with marketplace plans and many other types of insurance:

- Comprehensive breastfeeding support and counseling from trained providers, along with access to breastfeeding supplies, for pregnant and nursing women.

- Breast cancer mammography screenings every one to two years for women 40 years and older.

- Cervical cancer screening for sexually active women.

- Gonorrhea screening for women at higher risk.

- Well-woman visits to get recommended services.

Children

These preventive services must be covered for children under marketplace and most other health plans:

- Autism screening for children at 18 months and 24 months.

- Behavioral assessments.

- Blood pressure screening.

- Depression screening for adolescents.

- Developmental screening for children under age 3.

- Hearing screening for all newborns.

- Vaccines for illnesses, such as whooping cough, influenza, and chickenpox.

The pros of high-deductible health plans

Here are some of the benefits of an HDHP.

- Lower premiums: HDHPs typically have lower monthly premiums than health insurance plans with low deductibles and low out-of-pocket maximums. An out-of-pocket maximum is the most you might have to pay for covered services during the plan year.

- Potential savings: If you’re relatively healthy and generally don’t have medical expenses beyond annual physicals and screenings, you’re likely to save money by opting for an HDHP over a low-deductible plan. That’s because yearly checkups and screenings count as preventive services, which HDHPs typically cover before the deductible is met.

- HSA access: When you are enrolled in a qualified HDHP, you can contribute to an HSA. Contributions to an HSA are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses — such as hearing aids and prescription eyeglasses — are not taxed.

- Employer benefits: Some employers make HSA contributions for employees with HDHPs, which is another potential perk.

Effective Jan. 1, 2026, the OBBBA expands HSA eligibility by reclassifying bronze and catastrophic ACA marketplace plans as qualifying HDHPs. Bronze plans are the lowest-cost metal tier plans and typically come with higher deductibles. Catastrophic plans are very high-deductible options available to people under 30 and those with a hardship exemption.

The cons of high-deductible health plans

Yes, HDHPs keep monthly payments low. But there are some downsides you should consider, including the following.

- Large medical expenses: Since HDHPs generally only cover preventive care up front, an accident or emergency could result in very high out-of-pocket costs.

- Future health risks: Because of the costs, you may refrain from scheduling medical appointments, getting treatments, or purchasing prescription medications when they’re not covered by your HDHP. However, not getting care can lead to problems with your health. This could ultimately lead to needing more serious medical care, such as hospitalization, in the future.

- High deductibles: Many Americans have a relatively low amount of money in savings. A survey from KFF found that affording healthcare costs is difficult for about 2 in 5 adults. Among uninsured adults under age 65, that number rises to more than 8 in 10. Paying a high deductible can be especially challenging if you don’t have money set aside for medical expenses.

You can’t tell if or when a medical disaster may strike, so picking a health plan is always a bit of a gamble. If you need emergency care, you’ll have to pay your deductible up front, and you may have costs beyond that, up to your out-of-pocket maximum. So be sure to also look at a plan’s out-of-pocket maximum — and determine if you have access to that amount of money — before enrolling.

Is a high deductible or a low deductible better?

Whether a plan with a high deductible or one with a low deductible is better for you depends on your individual needs. HDHPs typically have lower monthly premiums. These plans are ideal for people who are generally healthy and do not expect to visit a healthcare professional often. An HDHP can also be paired with an HSA. By contributing to an HSA, you can take advantage of triple tax benefits and save money on healthcare now and during retirement.

Plans with lower deductibles may have higher monthly premiums. Like HDHPs, these plans usually cover preventive services up front, but you likely won’t have to pay as much out of pocket before your coverage kicks in for additional care.

In short, if an HDHP covers your annual preventive care and you think that’s all you’ll need in a given year, it may make sense to enroll. But if you’re worried about needing other kinds of care, it may make sense to pay more in premiums each month for a plan that offers more immediate access to comprehensive coverage.

High-deductible health plans vs. PPOs

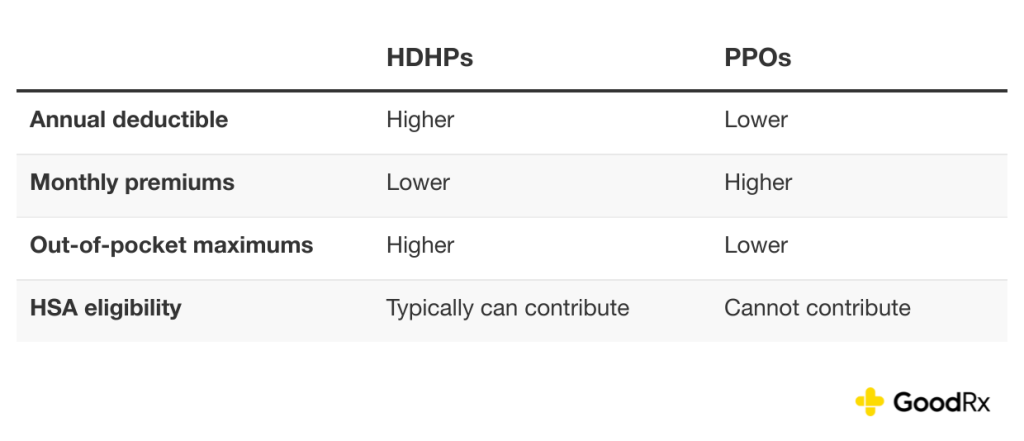

You may have the option to choose between an HDHP and a preferred provider organization (PPO) plan. These plans work differently, especially when it comes to costs. Here’s a chart comparing the features of these plans to help guide your decision.

Since HDHPs have a higher deductible and lower monthly premiums, you’ll have to pay more out of pocket for certain types of medical services before your coverage kicks in. PPOs, on the other hand, have a lower deductible and higher monthly premiums, and they have lower out-of-pocket costs for medical services.

With a PPO, you may have access to a larger pool of providers and hospitals, and some out-of-network coverage. Another PPO perk is that, in most cases, you won’t need your primary care provider’s approval to see a specialist or have a test done. In general, PPOs tend to offer more flexibility, but you pay for it in premiums.

The bottom line

A high-deductible health plan (HDHP) may be able to help you save money by allowing you to pay lower premiums and giving you access to a health savings account (HSA). This is especially true if you are generally healthy and the plan covers all of your routine care.

But HDHPs aren’t right for everyone. If you need ongoing medical care or face unexpected health issues, you may wind up spending more out of pocket with an HDHP. And while more Affordable Care Act (ACA) marketplace plans will qualify as HDHPs starting in 2026, your best bet is to crunch the numbers based on your individual financial and health status to see which options may be best for you.

This story was produced by GoodRx and reviewed and distributed by Stacker.