Carriers hold firm on fuel surcharges despite emerging US-Iran peace plans

The midpoint of June 2026 demonstrated that the world is moving away from broad, sweeping border surcharges toward highly targeted, regulatory trade walls. The United States actively advanced its strategy to replace expiring emergency surcharges with permanent Section 301 labor tariffs, while successfully utilizing massive Section 232 pharmaceutical duties to force international drug manufacturers into onshoring commitments. Simultaneously, the European Union acted to protect its internal market on two fronts: by closing the de minimis loophole with a new 3-euro flat fee on low-value online imports and by advancing the Turnberry trade deal to secure lasting tariff peace with Washington. Ultimately, the week proved that the global economy is functioning within a highly legalistic centralized trade architecture in the West, where access to prime consumer markets requires meeting strict labor, safety, and supply-chain origin mandates.

Freight Right broke down the state of the ocean and air freight markets this week.

This Week’s Ocean and Air Freight Markets

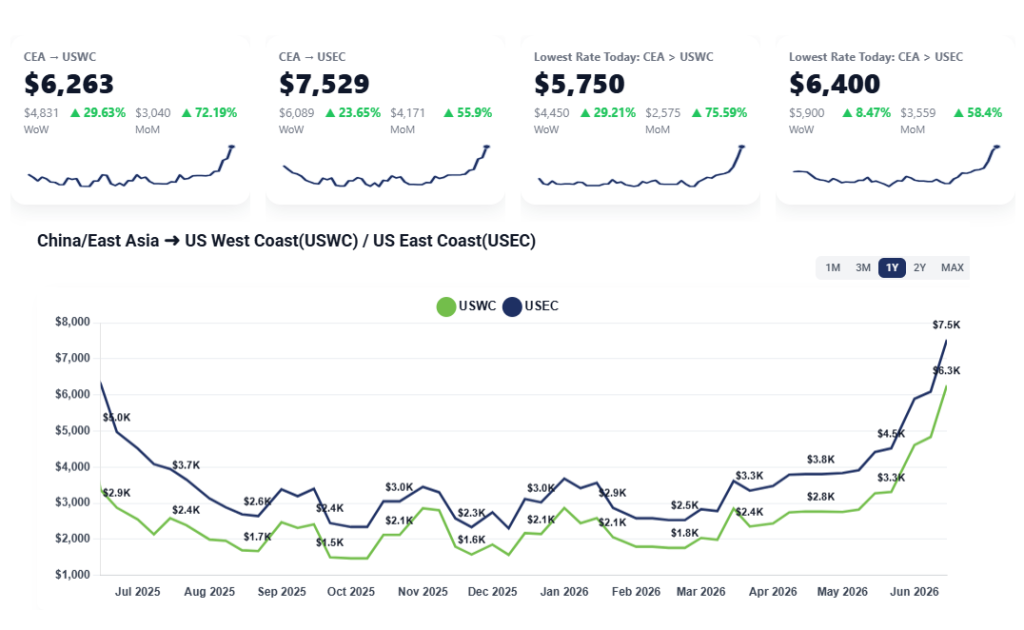

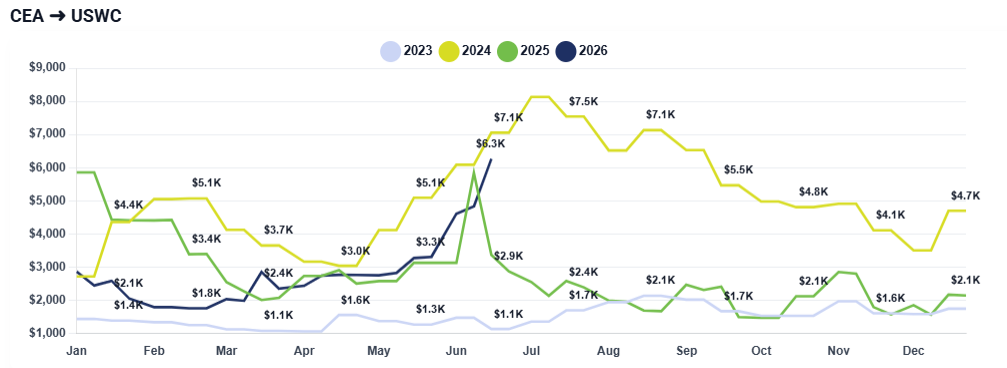

China-U.S. Ocean Freight Market: According to Freight Right’s TrueFreight Index, the transpacific ocean freight market has officially entered a higher pricing bracket. Over the past week, ocean freight rates from China to both North American coasts experienced a steep climb, driven by heavy volume increases in the first half of June and continued limits on available shipping space. The transpacific ocean freight market has officially entered a higher pricing bracket, confirming the expiration of $6,000 spot rates. Over the past week, ocean freight rates from China to both North American coasts experienced a steep climb, driven by heavy volume increases in the first half of June.

China/East Asia to U.S. West Coast: Spot rates have broken past previous thresholds and are now officially confirmed in the low $6,000s per forty-foot equivalent unit (FEU).

China/East Asia to U.S. East Coast: Rates to the East Coast have pushed even higher, settling firmly into the mid-$7000s per FEU.

For comparison, Gulf Coast rates are mirroring the East Coast in the mid-$7,000s, while inland moves to the Midwest (e.g., Chicago) have reached $8,000 to $8,400.

Freight Right’s Lowest Rate indicators are finding that importers can find spot rates as low as $5,750 from China to the U.S. West Coast and $6,400 from China to the U.S. East Coast. Talk to your freight forwarder about options available to you.

What Happened This Past Week

- Peak Season Front-Loading: Carriers reported a significant spike in cargo volumes during the first half of June. This surge is largely attributed to shippers front-loading their inventory early to avoid peak-season bottlenecks, which directly triggered carrier general rate increase (GRI) implementations for the second half of the month.

- Port Congestion and Rolled Cargo: Ongoing backlog from previous weeks continues to choke the network. This legacy congestion has triggered heavy rolling of bookings, severely degrading schedule reliability.

- Strict Dynamic Quoting: Due to the daily volatility in space availability, standard quotes are no longer guaranteed. Logistics providers are forcing a subject to roll and availability clause, as space secured one day is often entirely gone by the next.

Looking Ahead

The immediate outlook points to sustained upward pressure and prolonged volatility. Shippers should abandon expectations for a quick rate correction; carriers have just successfully pushed rates into the $6,000–$7,000+ range and will be highly resistant to lowering them, likely citing ongoing market uncertainty to justify keeping current fuel surcharges and base rates intact.

Furthermore, because booking backlogs are already stretching lead times out significantly, with some agents quoting the beginning of July as the earliest available space, shippers must plan and book several weeks in advance to secure equipment and vessel space. Even if the geopolitical situation in the Middle East stabilizes and a formal peace deal is signed by the end of the week, the lag in carrier operational adjustments means the earliest the market would see any tangible impact or relief on fuel surcharges would be late next week or early July.

This story was produced by Freight Right and reviewed and distributed by Stacker.