Coping with loss: Should you borrow for a funeral?

Saying goodbye to a loved one is never easy. The emotional toll of grief and the financial burden of funeral planning can be overwhelming. Many families struggle to find the money to pay for a funeral, and you often don’t get much time to figure out how you’ll pay.

The costs of a funeral can strain even healthy finances. A solution that works for some people is a funeral loan. It’s a personal loan for people who need a helping hand to cover the costs of saying goodbye.

Achieve explains how funeral loans work and what alternatives may be available.

Key takeaways:

- Funeral loans are personal loans that help you pay for funeral expenses over time.

- In some cases, a personal loan could be approved and funded within days after you apply. Sometimes that’s all the time you get to put a funeral together.

- In addition to paying for the service and burial, you could use the loan to cover related costs like airfare and hotels for family and friends attending the funeral.

What are funeral loans, and how do they work?

Funeral loans are usually unsecured personal loans. You get a lump sum of money up front when your loan is approved, and you repay it in equal monthly payments, usually over two to five years. There are typically very few restrictions on how you can use a personal loan. Once you receive the money, you could use it to cover expected or unexpected expenses, including final arrangements for a loved one.

Most people apply for funeral loans online, although you could also apply with your lender in person or over the phone if you’re more comfortable doing it that way. The lender will check your credit report and verify your income to decide how much you can borrow and what the interest rate on your loan will be.

If the lender approves your loan and you sign your loan documents, you could receive the money in as little as 24-72 hours.

Once you have the money in your account, you can pay for expenses such as:

- Embalming or cremation

- Casket or urn

- Burial plot

- Airfare and hotel expenses for people attending from out of town

- Event space rental

- Officiant fee

- Donation to the religious institution

- Obituary in your local newspaper

- Copies of the death certificate

Those expenses can add up fast. A funeral loan allows you to spread the costs out over time.

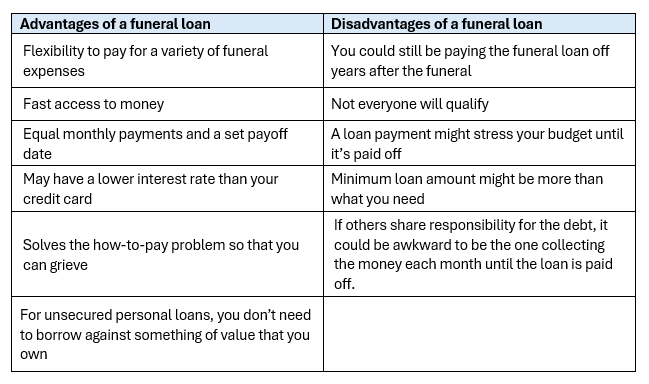

The pros and cons of funeral loans

Choosing the right funeral loan

A lot goes into choosing the right funeral loan. Here are a few important things to consider when deciding what funeral loan is right for you:

- How much do you need to borrow? Is the lender’s minimum more than what you need?

- Is there a prepayment penalty? If you borrow more than you need or family members help you repay the loan, can you pay it down ahead of schedule without a penalty?

- How long do you need to repay the loan? A two-year loan may have a lower interest rate or lower origination fee than a five-year loan.

- How much are the fees? An origination fee is the fee the lender charges for making the loan. It’s usually deducted from the amount you borrow, so the lower the origination fee, the more of the loan amount you receive. This fee may depend, in part, on your credit score.

Exploring alternatives to funeral loans

A funeral loan isn’t the only way to cover funeral expenses. Here are a few more tools that may help you pay for a funeral.

The Social Security Administration can pay a death benefit of $255 to a qualified surviving spouse or dependent child. While the amount may not seem like much, every little bit helps.

Your state or county might offer a grant to cover part of the funeral costs. The Pew Charitable Trust says 20 states have a cash grant to help low-income families pay for funeral or burial expenses. To find out if you are eligible for assistance, search “funeral grant in [your state or county]."

A secured loan may be easier to qualify for than an unsecured personal loan. A home equity loan or home equity line of credit is for homeowners who have sufficient home equity to borrow against. Equity is the difference between your home’s current market value and the amount you still owe on the mortgage (if you have a mortgage). You pledge your home as a guarantee that you’ll repay the loan. This lowers the risk for the lender, so they can be more flexible with qualification requirements. Secured loans often have a lower interest rate compared to unsecured loans and credit cards, and higher maximum loan amounts.

Providing support and comfort to your loved ones

It’s natural to feel overwhelmed when a loved one passes away, and those around you likely feel the same way. Dealing with funeral expenses, especially if they’re unexpected, can cause anyone stress. Figuring out how you’ll pay for those expenses could give you and your loved ones the space you need to focus on supporting each other.

This story was produced by Achieve and reviewed and distributed by Stacker.