Credit card debt hits $1.2T and shows no signs of stopping

At first glance, credit card debt numbers in the United States look enormous. Consumers owe an astounding $1.233 trillion on their credit cards, according to the Federal Reserve, and the average American credit card debt balance is $6,523, according to TransUnion, a major credit bureau. Debt is climbing even as wages struggle to keep up.

There’s no sign that credit card debt will meaningfully reduce any time soon. Rising credit card debt signals that more Americans are relying on borrowing to cover everyday expenses. That strain can erode household savings and slow economic growth as credit card interest rates stay stubbornly high.

Motley Fool Money analyzes what this rising debt means for Americans’ financial stability.

Average and total credit card debt reach new highs

How much credit card debt does the average American have? The average credit card balance is $6,523 as of the third quarter of 2025, according to TransUnion. That's a 2% increase from the previous year.

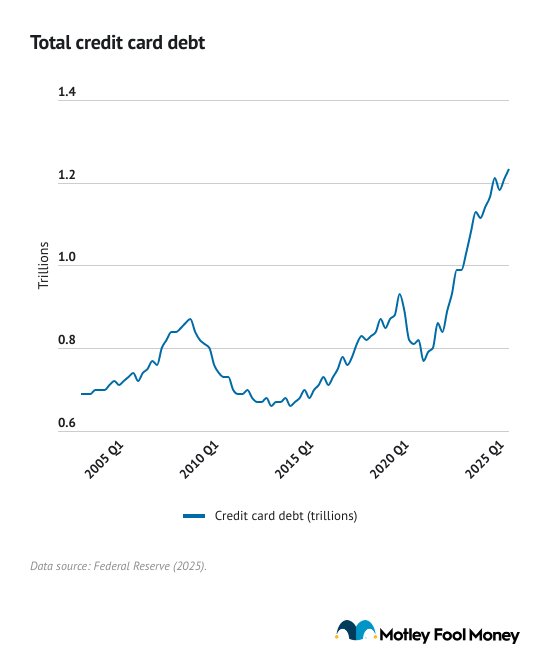

Meanwhile, total U.S. credit card debt rose to $1.233 trillion in the third quarter of 2025, up from $1.209 trillion in the previous quarter. Credit card debt fluctuated during the COVID-19 pandemic, but it began to steadily rise in 2021 as inflation took off.

Over the last decade, credit card debt has typically accounted for between 5.5% to 6.5% of total household debt.

The average American household has about $9,326 in credit card debt, according to the most recent U.S. credit card debt and household data. That’s higher than the average credit card account balance because multiperson households likely have more than one credit card.

Climbing credit card debt suggests that households are feeling the pinch of higher prices and borrowing costs even as consumer spending keeps the economy afloat.

Average credit card debt per household was calculated by dividing U.S. credit card debt in the third quarter of 2025 ($1.233 trillion) by the most recent data on the number of households (132.216 million as of 2024).

The states with the highest credit card debt

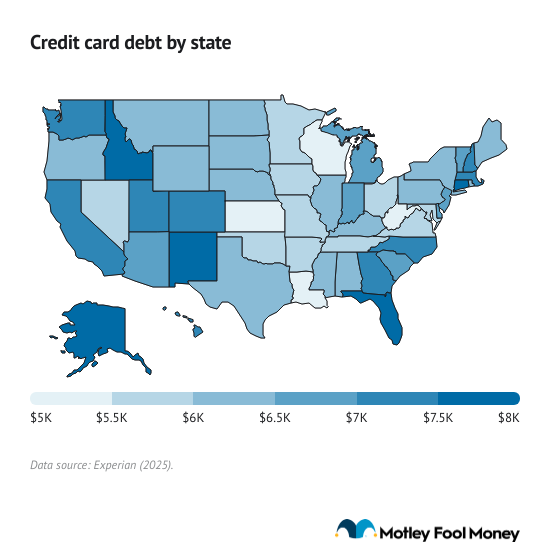

Alaska has an average credit card debt of $8,077, the highest of any state, according to Experian, a credit reporting bureau. Kansas and Wisconsin have the smallest average balances, at $5,329 and $5,370, respectively. The high variance in credit card debt among states highlights how local factors, such as the cost of living and household income, can influence borrowing.

States with higher average credit card debt, like Alaska and Florida, may reflect higher prices for everyday expenses or more expensive lifestyles and seasonal spending that relies on credit. Lower-balance states, such as Kansas and Wisconsin, could reflect a lower cost of living and more conservative credit use.

States with the highest credit card debt

- Alaska: $8,077

- Florida: $7,861

- New Mexico: $7,605

- Connecticut: $7,568

- Idaho: $7,560

States with the lowest credit card debt

- Kansas: $5,329

- Wisconsin: $5,370

- Louisiana: $5,399

- West Virginia: $5,427

- Missouri: $5,553

Credit card utilization rates remain steady despite rising debt

The average credit utilization rate is 29%, roughly level with previous years, according to Experian. That credit utilization rates — the percentage of a credit card limit used — have held steady despite overall credit card debt increasing and the average balance per account rising suggests that credit limits have been growing in tandem with balances.

The conventional wisdom is that a utilization rate below 30% has a positive impact on credit scores, so consumers are doing well managing their credit cards despite holding higher balances.

Credit card interest rates stay high despite Fed cuts

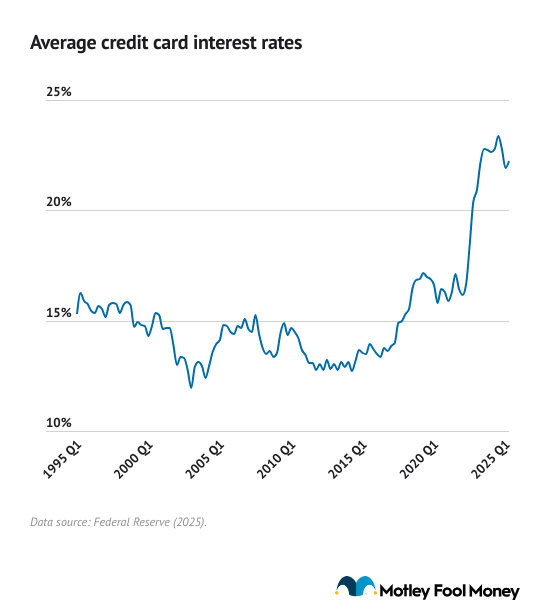

The average credit card APR on interest-bearing accounts is 22.25% as of the third quarter of 2025, according to the Federal Reserve. Credit card interest rates have risen quickly since 2021, as the Federal Reserve hiked its benchmark interest rate. Those rates have remained above 20% since November 2022 and have yet to return to the more standard 13% to 16% range, despite the Federal Reserve cutting interest rates.

Interest-bearing accounts include all credit cards that charge interest. It excludes credit cards that aren't charging interest at that time, so 0% intro APR credit cards don't count until the introductory period ends. That could skew the average higher. Interest-bearing accounts make up a significant chunk of card issuers' earnings.

Credit card delinquencies are on the rise

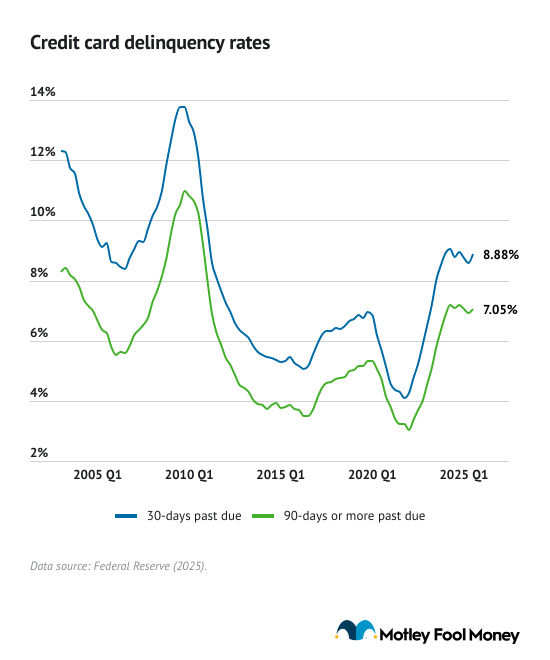

Data from the Federal Reserve shows credit card delinquencies — balances past due by 30 days or more — continue to grow.

The 30-day past-due delinquency transition rate for credit cards rose to 8.88% in the third quarter of 2025, up from 8.58% in the previous quarter. The serious delinquency rate, in which balances are 90 days or more past due, was 7.05%, up from 6.93%

Overall, 12.41% of credit card balances are 90 days or more delinquent, up from 12.27% in the second quarter.

Sustained growth in credit card delinquency rates could point to underlying weakness in household finances. Credit card balances and interest can compound and don’t have a repayment schedule, unlike other lines of credit. As a result, households in credit card debt often end up paying mostly interest each month, making it harder to reduce their actual balance and leaving less money left over in their bank accounts.

Who’s carrying America’s credit card debt?

Credit card debt varies by age, race and ethnicity, and income, revealing which groups may be at the greatest risk of financial strain.

Gen X, for example, has the highest credit card balance at $9,600, followed by millennials at $6,961 and baby boomers at $6,795, according to Experian. Gen Z, with much lower purchasing power, and the Silent Generation, with less disposable income, each have under $3,500 on average on their credit cards. Gen Xers are in their prime earning years and are juggling the expenses of raising families, buying homes, and other financial responsibilities. Their relatively high average balance is a reflection of that.

Looking at race and ethnicity, white Americans hold the highest median credit card balance at $3,000, but they are also the least likely to have credit card debt, which is held by 42% of those households, according to the Federal Reserve. Median balances are lowest for Black and Hispanic households at $1,700, but 57% of those households carry credit card debt. These gaps reflect income disparities and access to credit, and highlight which communities are most vulnerable to high credit card interest rates.

Americans in higher income brackets carry larger credit card balances on average; however, the share of people in debt peaks among those with an average or slightly above average income. The top 10% of earners have a median balance of $6,000, yet only 25% of them carry credit card debt. In contrast, more than half of households in the 40th-80th income percentiles carry balances, though their averages are $2,000-$3,000 lower.

That dynamic shows how middle-income households are more financially stretched, and highlights how reliance on credit can expand the wealth gap between affluent earners who can easily pay off balances and those managing everyday expenses with the potential to rack up high-interest debt.

How to get out of credit card debt

Owing money to a credit card issuer isn’t uncommon: The data shows that more Americans are falling behind on their credit card payments.

Motley Fool Money personal finance expert Joel O'Leary suggests these tips to help beat credit card debt:

- Pause interest with a 0% intro APR card: Transferring balances to a 0% intro APR card can stop interest charges temporarily, letting payments go directly toward principal. Just watch for transfer fees (typically 3–5%) and note that good credit is usually required.

- Pick a payoff strategy: Use the debt snowball method to build momentum by clearing the smallest balances first, or the debt avalanche method to save more by targeting high-interest debts first—both are proven ways to pay down credit faster.

- Trim spending and redirect savings to debt payments: Cutting even $100 a month by canceling unused subscriptions, switching to a cheaper phone plan, or cooking at home can help chip away at balances more quickly.

- Seek nonprofit guidance: Certified credit counseling agencies like Money Management International (MMI) and the National Foundation for Credit Counseling (NFCC) offer free, trusted advice and customized repayment plans without sales pressure.

Rising credit card balances, high interest rates, and growing delinquencies underscore the challenges that many households face in managing debt, making careful financial planning more important than ever.

This story was produced by Motley Fool Money and reviewed and distributed by Stacker.