The hidden costs and considerations of refinancing your mortgage

For many homeowners, refinancing sounds like an easy way to save money, lower payments, or free up cash. After all, as interest rates fall, why not replace your existing loan with something cheaper?

A lower rate doesn’t automatically mean a better deal, and in some cases, refinancing can actually cost more than it saves. Splitero explains how understanding the timing, costs, and alternatives can help you avoid common pitfalls.

Waiting periods before refinancing

One factor many homeowners overlook is that most mortgages come with built-in waiting periods, sometimes referred to as a “seasoning” period, before you’re eligible to refinance.

- Conventional loans: Typically require about six months before you can refinance.

- FHA loans: Can have a waiting period of anywhere from zero to six months, depending on the type of refinancing option, but may require a history of up-to-date payments.

- VA loans: Usually require a 210-day waiting period, but it may vary depending on the type of refinancing option you pursue.

Even if you meet those timelines, refinancing too soon can mean paying thousands in fees that wipe out any short-term savings. Just because you qualify doesn’t always mean it’s the right financial move.

When lower rates don’t equal savings

A common misconception is that a lower rate automatically makes refinancing worthwhile, but it depends on your personal situation. If you’re close to paying off your mortgage, restarting the loan term could lead to paying more in interest overall — even with a smaller monthly payment.

When considering the potential cost of refinancing, homeowners should factor in closing costs, which often include:

- Origination fees: A percentage of the loan amount to cover processing.

- Appraisal fees: Required to reassess the value of your home.

- Other administrative costs: Title searches, inspections, and legal fees.

These expenses can add up quickly. If the savings from refinancing don’t outweigh the upfront costs, sticking with your current loan could be a better decision.

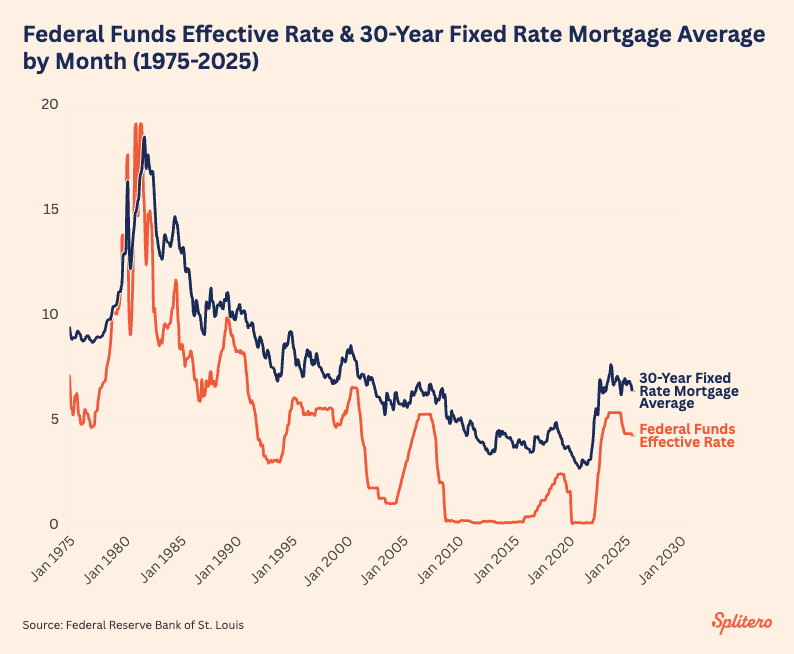

Interest rates in 2025

In mid-September 2025, the Federal Reserve cut interest rates for the first time since December 2024, bringing the federal funds target range down to 4–4.25%. Even so, mortgage rates remain significantly above the ultra-low levels seen in 2021.

The monthly average rate for a 30-year fixed-rate mortgage in September 2025 was 6.35%, which is lower than the June 2025 average of 6.82% but still high compared to 2.90% in September 2021.

The risks of cash-out refinancing

Cash-out refinancing, which allows you to borrow against your home equity and take out cash, can be tempting. Homeowners often use these funds for renovations, debt repayment, or major purchases. If you’re considering this option, it’s important to evaluate the potential risks:

- Cash-out refinances often come with higher interest rates and fees than traditional refinancing, as lenders typically view them as riskier than conventional refinances.

- Extending your loan term may result in higher interest payments over time.

- By converting unsecured debt (like credit cards) into secured debt, you put your home at risk if you fall behind on payments.

For homeowners with substantial equity in their homes, refinancing for cash can be an appealing option. According to the Intercontinental Exchange, accessible home equity reached a record high in Q2 2025, with homeowners entering Q3 holding $11.6 trillion in accessible equity. During Q2, cash-out refinances accounted for more than half (59%) of all refinance transactions.

However, Intercontinental Exchange reports that 70% of these homeowners ended up with a higher interest rate than they had before. Homeowners leveraging a cash-out refinance also saw their monthly payments increase by about $590.

For some, the trade-off may be worthwhile, but it’s essential to weigh the risks carefully.

Barriers to refinancing

Common roadblocks to refinancing your mortgage can include:

- Poor credit that prevents lenders from offering favorable terms.

- Insufficient home equity, which can reduce your borrowing power and, in some cases, disqualify you completely from some types of refinancing.

- Unconventional income streams that don’t meet lender requirements.

- Property liens or lender-specific rules can also block approval.

Not everyone qualifies for a refinance. Access to traditional lending is becoming increasingly concentrated among borrowers with higher credit scores. Recent data from the Federal Reserve Bank of New York indicate that most mortgage originations are made to households with credit scores above 600, with many clustered in the 700–760 range.

According to Experian, less than three-quarters of consumers had credit scores of 670 or higher in 2024. This could mean that many homeowners, often those facing the most significant financial need, are shut out of options like HELOCs and home equity loans.

Homeowners with credit scores below 600 may be eligible to refinance an FHA or VA loan, but poor credit can result in higher interest rates. These homeowners may have significant home equity but lack the credit profile or income documentation that today’s lenders require.

These hurdles underscore the importance of preparation before pursuing refinancing.

How to improve your eligibility to refinance

If refinancing isn’t possible now, there are steps you can take to improve your chances later:

- Pay bills on time to raise your credit score.

- Reduce outstanding debt to improve your debt-to-income ratio.

- Maintain steady, documented income.

- Resolve any property liens before applying.

- Shop around with multiple lenders for the best terms.

Even small improvements in your financial profile can make a big difference in eligibility and costs.

Considering alternatives: Home Equity Investments

For homeowners who want to access their equity but don’t want to take on new monthly payments, alternatives like Home Equity Investments (HEIs) are worth considering. An HEI provides a lump sum of cash today in exchange for a share of your home’s future appreciation.

Unlike refinancing, HEIs don’t require monthly payments, employment verification, or traditional debt qualifications. In some cases, a credit score as low as 500 may be sufficient to qualify.

Example: Imagine a homeowner with a locked-in 3% mortgage rate. They need $40,000 for home improvements, but don’t want to refinance into a loan with a 6.3% rate. An HEI lets them access cash while keeping their existing mortgage terms intact.

This option isn’t for everyone, but it is one way to utilize equity without the risks associated with refinancing in a high-rate environment.

Should you buy now and refinance later?

Many buyers choose to purchase a home when it fits their needs, even if the rates are higher, with the plan to refinance later if conditions improve.

This approach can work, but it’s important to remember that refinancing down the road isn’t free. Potential costs include:

- Origination fees charged by lenders.

- Prepayment penalties may apply if your current loan has such provisions.

- Higher rates and fees if you choose a cash-out refinance later.

Buying the right home now can still be the right decision, but homeowners should go in with a clear understanding of future costs.

Understanding your options

Refinancing can be a powerful financial tool, but it isn’t always the right choice. Built-in waiting periods, hidden costs, and the risks of restarting a mortgage can all turn a “better deal” into a more expensive one. Cash-out refinancing may provide access to cash, but it often comes with higher fees and risks.

For homeowners who need flexibility, alternatives such as Home Equity Investments may offer a way to access equity without incurring additional debt. The key is to carefully weigh your options, improve your financial readiness, and choose the approach that best aligns with your long-term goals.

This story was produced by Splitero and reviewed and distributed by Stacker.