Veteran debt relief grants: Your guide to financial assistance programs in 2026

For veterans with debt, lots of help is available. Government, nonprofit, and private organizations offer a range of programs to help you get your finances back on track.

Veteran debt relief grants don’t have to be repaid. That’s just the tip of the iceberg of the debt relief options open to veterans. You’ve got access to pensions and other benefits, housing assistance, education, counseling, debt settlement, and even legal protection.

In other words, debt relief comes in many forms. Debt relief may not be something that directly pays off your debt. Anything that improves your income or reduces your expenses could free up more money to put towards paying off debt.

Being open to the different forms of veteran debt relief means there can be a broader range of assistance available to you. In this article, Freedom Debt Relief explores what’s possible to help you find the type of debt relief that fits your situation.

Key Takeaways:

- Grants are just one of several forms of veteran debt relief.

- You may be eligible if you served in the military, even if you didn’t serve in a combat zone.

- The nature of your discharge may affect your eligibility.

- Other forms of financial assistance include pensions, loans, GI Bill education benefits, and disability compensation.

- Credit counseling, debt management plans, and negotiated debt settlement are all possibilities for debt relief.

- Veteran debt relief is available from the government, nonprofits, and private companies.

Government-Sponsored Veteran Debt Relief Grants

In return for your service to your country, the government provides different types of financial assistance. Here are some key ways the government offers financial help to veterans, along with examples of programs worth looking into.

The Veterans Administration

The Veterans Administration (VA) is the primary organization that coordinates benefits for U.S. military veterans. Examples of financial help include:

- Military pensions

- Disability compensation

- Housing assistance

- Grants for adaptive homes and vehicles

- GI Bill education and training funding

You may find ways to improve your income or reduce your expenses, which could give you some breathing space in your budget to attack debt.

If you have VA debt from a previous loan, benefit overpayments, or medical co-payments, you can apply to the VA for debt relief by filling out VA Form 5655. You’ll provide information about your income, expenses, and other financial circumstances. The VA will review your situation and decide if you qualify for a modification of your payment schedule. They may reduce the amount you owe.

You might be wondering if veteran debt relief programs will affect your VA benefits. It’s possible that some programs will. If you receive VA benefits and have a VA debt, you may have to give up some or all of those benefits until the debt has been paid. Another possibility: The VA may approve another repayment or debt relief option.

The Department of Defense

If you’re an active service member, the Department of Defense (DoD) provides information on financial assistance and other benefits through the website MilitaryOneSource.mil.

In addition, the DoD has specific official relief organizations for different branches of the military:

- Army Emergency Relief

- Navy-Marine Corps Relief Society

- Air Force Aid Society

- Coast Guard Mutual Assistance

Can veterans with less-than-honorable discharges qualify for debt relief programs?

Having less than an honorable discharge could affect your eligibility for government veterans benefits. In particular, a dishonorable discharge often bars you from receiving those benefits.

Even with a dishonorable discharge, you may be able to find help. You can try nonprofit organizations or private debt relief or credit counseling firms.

State-specific programs

States typically have their own departments of veterans affairs that coordinate veterans assistance programs there.

In some cases, those programs provide grants to nonprofit organizations that support veterans in the state. Programs sometimes provide support directly to veterans.

For example, New York State's Department of Veterans’ Services provides up to $2,000 in emergency housing assistance. California offers property tax exemptions for veterans.

These programs vary widely from state to state. In some cases, your city or county may also offer veterans programs. When you have to choose between paying off debt and meeting other expenses, any form of financial support can help the numbers add up.

In short, while the federal government provides a significant amount of support to veterans, don't limit yourself to that one source. You may find additional help locally.

When applying for any veterans program, be ready to provide a copy of your Form DD214. This form details the character of your discharge from the service. You may also need other information about your service record, which you can obtain through the National Archives. You can make this request online through the eVetRecs website.

Nonprofit Organizations Offering Veteran Debt Assistance

Many nonprofits can help with counseling, financial assistance, and other programs for veterans struggling with debt.

Here are some examples:

- The Bob Woodruff Foundation provides grants to organizations that help veterans. Their emphasis is on access to food, housing, employment, and healthcare.

- Disabled American Veterans (DAV) helps veterans fill out claims for benefits. It also holds job fairs to help veterans find employment and provides free rides to medical appointments.

- The Gary Sinise Foundation’s Restoring Independence Supporting Empowerment (RISE) program builds specially adapted housing for wounded veterans.

- Operation Homefront has a Critical Financial Assistance Program that helps veterans who are having trouble making ends meet.

- USA Cares provides direct emergency financial assistance to veterans.

- Warrior Rising provides funding and guidance to veterans starting their own businesses.

Thousands of other local and national nonprofit organizations are dedicated to helping veterans. They specialize in helping with various types of needs.

Before applying to an organization, do a little research. Find out about the organization's reputation. When in doubt, steer toward older, more established organizations instead of start-ups.

Research the programs and areas of emphasis. Try to find ones that are aligned with your situation, based on your service, physical abilities, and financial needs.

Generally, there's a process to follow when applying for aid. Be patient, learn the process, and provide whatever information is required. Also, ask about the normal response time so you'll know when you should follow up.

As in the military, there's generally a reason for this type of process. Doing things by the book will improve your chances of success.

Specialized Debt Relief for Disabled Veterans

If you were disabled as a result of your military service, you may have special financial needs. Several nonprofits provide financial assistance to disabled veterans. Still, the best place to start is by finding out about VA disability benefits.

Benefits are typically based on the severity of your disability and how it was incurred. The VA assigns a disability rating based on the degree to which your condition limits you. If you have more than one medical condition, the impacts of these conditions are combined to calculate your disability rating.

The VA provides a disability benefit based on this disability rating and considers whether you have family members who are financially dependent on you. Here’s how to file with the VA:

- Start by filing a disability claim, which you can do online. You'll need information from your medical records and supporting statements from people familiar with your situation.

- Be as thorough as you can. It's not just a question of whether you get approved. The size of your benefit may depend on making sure the VA has all the relevant information.

- Be prepared to wait after filing. The VA takes about 107 days to make a decision about disability claims, and they may request more information. The faster you can provide information, the sooner the application can move along.

- The time and effort could prove well worth it if your disability benefit allows you to pay off debt and meet your other expenses.

Alternative Debt Relief Options for Veterans

So far, we’ve detailed financial assistance from grants, pensions, and disability benefits. You can find other types of debt relief to make your debt payments easier to manage.

Here’s an overview of these types of debt relief.

Servicemembers Civil Relief Act protections

The Servicemembers Civil Relief Act (SCRA) provides some protection to veterans when military service limits their ability to meet their financial obligations.

Debt relief available under the SCRA may include:

- Reduced interest rates on existing debt

- Deferred income taxes

- Eviction prevention

- Termination of leases

- Repossession prevention

The SCRA is wide-ranging, and it’s a good idea to seek help from a military legal assistance office. Talk to someone familiar with the law and your circumstances to figure out if the SCRA can help with your financial problems.

VA debt payment options

If you have a VA mortgage, some debt relief options might make those payments more manageable:

- A repayment plan with reduced monthly payments.

- Debt settlement, through either a compromise offer or a debt waiver.

- A VA interest rate reduction refinance loan can lower the interest rate you're currently paying on your mortgage.

- Even if your mortgage isn't a VA loan, a cash-out VA refinance loan might allow you to refinance other debts at a lower interest rate, and on a repayment timeline that works for your budget.

How long does the application process for VA debt relief grants typically take?

VA debt relief is more likely to be a loan, a reduction in payments, or a waiver of some of the amount owed, rather than a debt relief grant. The time this takes varies depending on the complexity of your case and VA staffing issues.

Once you request debt relief from the VA, you should immediately receive written confirmation that the request has been made. After that, the VA will notify you of the date of any hearing, if applicable, or of the decision in your case.

Credit counseling

Credit counseling from nonprofit credit counseling agencies could help you get a handle on your finances if you agree to complete their debt payoff program. They may:

- Review your financial situation

- Set up a debt management plan for you

- Negotiate with your creditors to lower interest rates

These services are generally applied to unsecured debt, which includes credit card debt, medical debt, and personal loans.

Credit counselors typically charge a fee for their services. The fee amount is based on the counselor and the services you need.

Negotiated debt settlement

Another debt relief tactic available to veterans is debt settlement. Debt settlement is a negotiated agreement for a creditor to accept less than the full amount you owe.

Why would a creditor do this? They may realize it's in their best interest if you have little money and other creditors are also trying to get money from you. It helps if you can show a good reason why you became unable to pay your bills.

You could attempt this type of debt negotiation on your own or hire a professional debt settlement company.

The main benefit of hiring a professional is that they've done this kind of negotiation successfully many times. They know how to approach creditors and the kind of offer a creditor is likely to accept.

Debt settlement will appear on your credit history, and any amounts forgiven may be treated as income for tax purposes. If the total value of your debt is greater than the total value of what you own at the time you settle your debts, you won’t have to pay income taxes on the forgiven amounts.

Debt settlement could significantly reduce what you owe and give you a financial reset.

Bankruptcy

Bankruptcy is a legal process for dealing with debt. In bankruptcy, you demonstrate to a court that you can’t pay all your debts. The court then decides how to divide your assets among your creditors. Depending on the type of bankruptcy you file, you might propose a repayment plan that the judge approves.

This puts your finances in the hands of a bankruptcy judge. Once the process is complete, you should be protected from any further collection attempts for the debts included in your bankruptcy. A bankruptcy will stay on your credit record for seven to 10 years. Bankruptcy might be the best way to get on a better financial track if there's no other way of paying your debts.

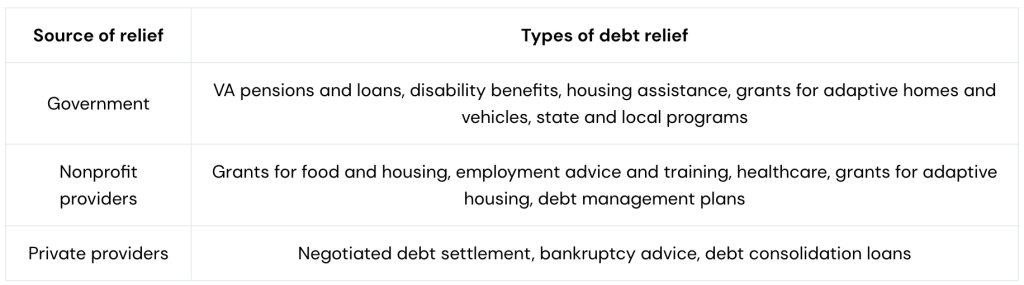

Debt Relief Guide for Veterans

Veteran debt relief grants and other assistance are available from a variety of sources. Here’s a summary of those sources and the types of debt relief available.

What documentation do you need to apply for veteran debt relief grants and other assistance?

Different organizations have varying requirements. If the program is designed for veterans, you'll likely need a copy of your form DD214, showing the nature of your discharge. You may need other records from your military service, along with your medical records.

Success Stories and Case Studies

America's veterans have a proud history of achievement. That includes overcoming financial obstacles as they transition to civilian life. Here are some examples that have been documented in national news stories:

- One veteran amassed $110,000 in debt after leaving the military in 2010. A debt relief program helped her pay off $70,000 of that debt. She could then pay down the remaining $40,000 on her own.

- Another veteran paid off $37,000 in debt with the help of a debt relief program. Getting rid of that debt enabled her to get a VA loan to buy a home.

- Using more than one debt relief tool can help get the job done. One veteran used military disability compensation to get started repaying $25,000 in credit card debt. After that, the vet used a debt consolidation loan to reduce the cost of that debt.

Now it's time to write your own success story. You don't have to be defeated by debt. With the right help, you can be victorious.

This story was produced by Freedom Debt Relief and reviewed and distributed by Stacker.