What does it cost, emotionally and financially, to build a life together?

“Will you be my joint account holder?”

It’s not exactly a rom-com line — but for many couples, love isn’t just about chemistry or commitment. It’s also about the mish-mash of money that tends to come with building a life together. That means navigating what’s yours, what’s ours, and how we make sense of it all.

To understand how people are actually navigating the intersection of love and money, Mercury, a fintech platform that offers business and personal banking services*, surveyed 1,400 U.S. adults in committed relationships — spanning generations, income levels, and financial arrangements. The “New Economics of Modern Love” report uncovers more about their choices, feelings, and behaviors around money — including who’s got the account passwords.

Methodology: This report is based on a January 2026 online survey of 1,400 U.S. adults in committed relationships, including 1,200 respondents who share or coordinate finances and 200 who do not. The sample was provided by Sago, a research panel company. Numbers are rounded to the next whole digit; percentages may not add up to 100%.

How people actually think about money — before it ever becomes ‘ours’

Across the survey, respondents most often describe money as:

- A source of security (48%)

- A tool to build the life I want (47%)

- Something I need to manage carefully (43%)

While the first two tended to become more true as people had more money, that last one held pretty evenly, regardless of income, gender, and generation — though people with the most money (annual household incomes over $200,000) or time on Earth (for Mercury’s survey, this was respondents in the Baby Boomer generation) were least likely to be concerned with careful cash management.

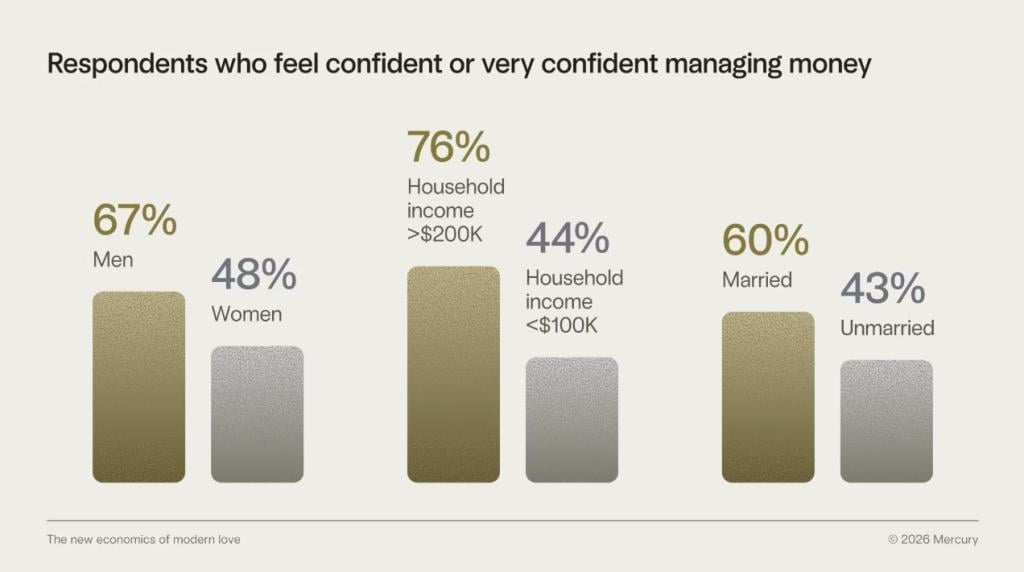

Most people feel confident managing their day-to-day money

57% of respondents say they feel confident or very confident managing money in their day-to-day lives. But that confidence is a bit unevenly distributed:

- Men (67%) report higher financial confidence than women (48%).

- Confidence increases substantially with household income (44% for couples with HHI under $100,000 versus 76% for those with HHI over $200,000).

- Married respondents (60%) are more likely to report high confidence than unmarried ones (43%).

Generationally, Gen Z (59%), Millennials (61%), and Baby Boomers (58%) had a lead on Gen X (50%) in feeling financially confident or very confident.

Notably, across the board, respondents were more likely to feel confident navigating money with a partner (73%) than managing it alone.

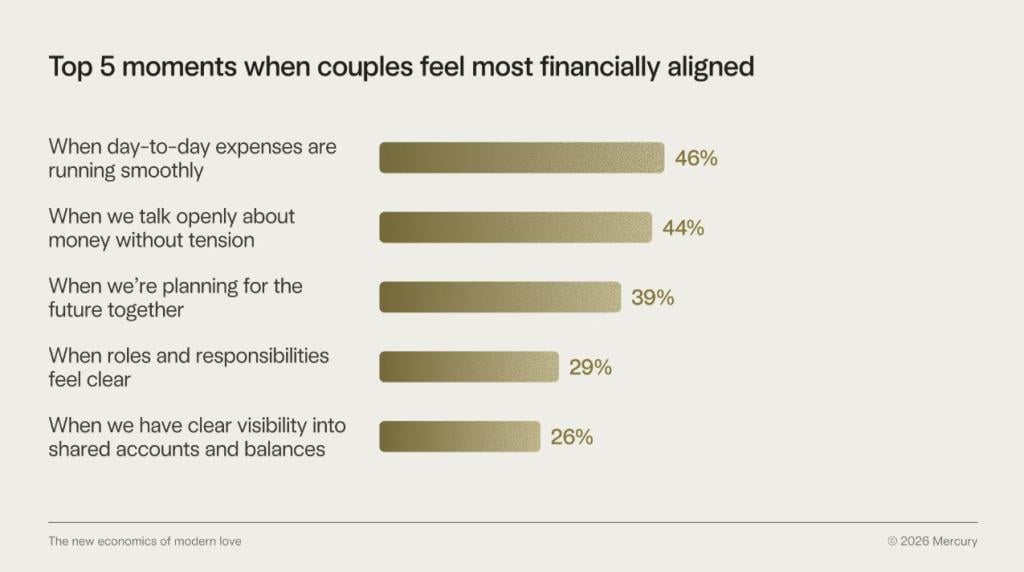

Contributing to that is a somewhat variable sense of financial alignment. Only around a quarter of respondents (27%) reported they rarely feel financially misaligned with their partner. So when do things work out best?

Older generations seemed to have a different joint relationship with financial future planning: Gen X and Boomer respondents (both 35%) highlighted this less often than Millennials (43%) and Gen Z (46%) as a moment of greatest alignment. Alignment on responsibilities also seemed to have decreasing impact by age, with it being a key alignment area for Gen Z (38%) and gradually declining to 23% for Boomers.

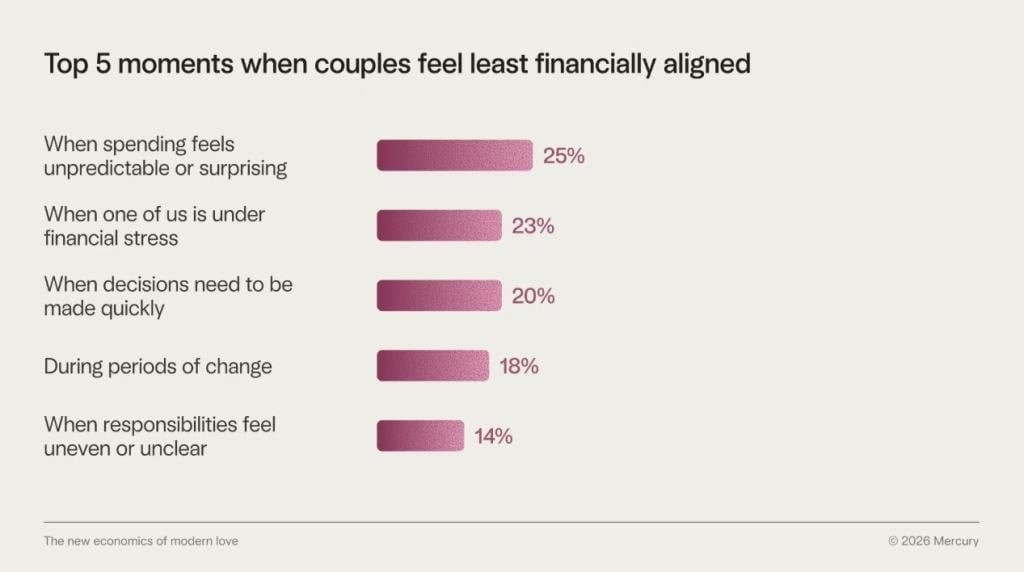

On the other hand, the top factors that came through around misalignment were all versions of situational rockiness and more consistent across demographics.

While respondents highlighted significant financial compromises around all kinds of things — from the cars they buy to their investment strategies to whether or not they’re buying Prada — housing-related costs were the most common. 1 in 7 respondents noted compromises around things like the cost of a down payment or mortgage, home renovations or improvements, HELOCs, and deciding on housing location, price, and size.

When sharing money starts to make sense

There was also no single moment when money flipped from “mine” to “ours.” (And for 3% of couples who coordinate or share money, it still doesn’t feel shared, regardless.) But two main points of transition did stand out as frontrunners:

- 45% say money began to feel shared when they got married.

- 28% say it happened when they moved in together (and this spikes to 52% for unmarried couples).

Gen Z (11%) were the most likely among respondents to say money felt shared before they moved in with a partner. They were also more likely than other generations (42%) to pin the shift on when they moved in together, whether or not they were married now. Gen X (47%) and Baby Boomers (63%) were much more likely to point to marriage as the defining moment, while Millennials were fairly split between moving in together (32%) and marriage (38%).

Taken together, these numbers point to our shared relationship with money coinciding with moments when coordination becomes more consequential — legally, logistically, or practically. And that doesn’t mean there was a reluctance to share prior. It might just be that the circumstances didn’t really call for it yet.

Most people feel their financial arrangements are fair, but lower-income households are less likely to agree

Overall, 80% of respondents say their financial arrangement feels some degree of fair. Men found things a little fairer at 87%, versus 74% of women. That sense of fairness dipped to 70% for those with the lowest household income (under $50,000).

And respondents were most likely to report that responsibilities were about equal between them and their partners (45%), though Baby Boomers (54%) were the most equitable on this front, ranking 11 percentage points ahead of all other generations.

That said, it certainly wasn’t the case for everyone. In relationships where things didn’t feel quite so equal, perceptions of leadership had meaningful skews by gender:

- Men self-identified as the financial “leader” in their relationship almost two times as often as women (38% vs. 21%).

- On the other hand, only 16% of women say their partner leads.

If we assume same-sex couples account for a few percent of the relationships reflected here, that’s still a sizable gap in how men and women perceive the roles in their financial power dynamic.

Women were also more likely than men to say they each lead different areas of their shared financial lives. Nearly half of respondents (48%) say these financial roles happened organically, while just 16% say they were explicitly discussed and 33% say it’s some mix of the two. (The rest said things were still evolving.) Men and women were very aligned here.

And, regardless of who’s in charge or how they got there, when asked what would happen if partners switched financial roles for a month, things were a bit all over the map: People were pretty split on whether it would be stressful (23%) or easy (21%), and whether their partner could use their financial apps (20%).

The study did uncover one clear standout: Women seem to be the password keepers. Or, at least, they were quite a bit more likely than men (22% vs. 14%) to say their partner wouldn’t know where all the passwords are.

Big expenses and future plans spark money talks

The report found that some money moments tend to get couples talking, with 57% of married couples responding that a large or unexpected expense is the most likely event that triggers money conversations. Half of Gen Z (50%) and Millennials (51%) noted planning for the future as their number one trigger for money conversations, versus 37% across both Gen X and Baby Boomer couples. Gen Z were two times as likely as Boomers (32% vs. 16%) to tout stress or tension around money as typical conversation triggers.

Gen Z were also least likely to have conversations around large or unexpected expenses — just 39%, compared to 56%-60% for all other generations.

The good news is that only 10% of respondents felt their partner often spends too much money — a number that held pretty steady across the board. While plenty of respondents (36%) have occasional misgivings, a majority (52%) don’t see any issues with their partner’s spending.

That said, most respondents (67%) say they have a spending threshold where they feel a purchase should be discussed first. Most commonly, this was between $100 and $499 (32%) or $500 and $999 (25%). And, perhaps, unsurprisingly, the threshold scaled pretty linearly with income.

What it really takes to build a financial life together

Feeling comfortable together financially seems to have less to do with any specific financial setup, merging of money, or dollar amount in the bank (though the latter doesn’t hurt). Instead, it’s more about whether expectations are clear and decisions are made with context. Regardless of age, gender, income — and any of the awkward human bits around perception, power dynamics, the lot of it — the study found that people felt most confident handling finances with their other half.

Maybe the key to modern financial partnership is something timeless: building a life with someone you love, and committing to the ongoing work of making money easier to live with together.

*Mercury is a fintech company, not an FDIC-insured bank. Banking services provided through Choice Financial Group and Column N.A., Members FDIC.

This story was produced by Mercury and reviewed and distributed by Stacker.