50-year mortgages won’t address the issues facing first-time buyers

President Donald Trump suggested the idea of 50-year mortgages to make home buying more affordable for Americans. It’s not the first time this idea has been tossed around, and it’s even been tried before.

The idea behind a long mortgage is to save borrowers some cash by reducing their monthly payment. And it would do that, but the way mortgages work, it doesn’t actually save you money. Finder.com explains how this type of mortgage would function and what it would mean for buyers.

How a 50-year mortgage would work

Most mortgages use an amortization model, also known as being front-loaded.

Front-loaded means that the majority of your monthly mortgage payments go to paying down interest in the first few years of the loan. Over time, more and more of your monthly payments will be allocated toward your actual loan balance.

For example, let’s say you buy a $400,000 house, and your 50-year mortgage has a 6% interest rate. Your monthly mortgage payment would be $2,105.62.

With mortgages being front-loaded, this means $2,000 of your first payment goes toward interest, and $105.62 goes toward your principal. With a 50-year mortgage, it will take nearly 20 years before half of your monthly payment goes toward your principal.

And compared to a 30-year mortgage, stretching a mortgage to 50 years on a $400,000 home only reduces your monthly payment by $292.58.

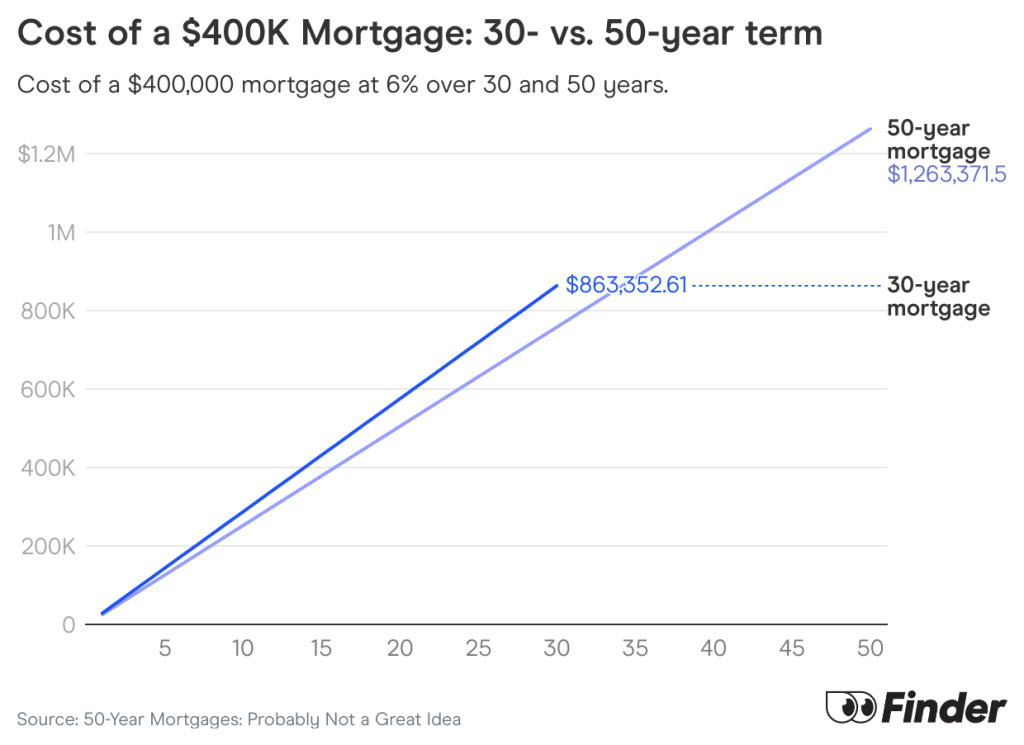

50-year mortgages can mean double the interest

Using the same example of a $400,000 home with a 6% interest rate, here’s how much you would pay in interest based on the loan term:

- 30-year mortgage: $463,352.76 total interest

- 50-year mortgage: $863,371.51 total interest

Paying nearly double the interest and being locked in a mortgage for 50 years does not seem worth it to reduce a mortgage payment by less than $300 each month.

50-year mortgages are also a nightmare for equity

Home equity is the difference between a home’s market value and how much you owe on the house.

With a 50-year $400,000 mortgage, it would take over 38 years to build 20% in home equity (assuming your home value stays the same and you don’t make extra payments).

These numbers matter because to refinance your mortgage or avoid paying mortgage insurance, you need at least 20% equity in most cases.

So for nearly 40 years, you’ll have significant negative equity on that home loan, which isn’t an ideal place to be.

Super long mortgages aren’t a new idea, either

In the late 1980s, Japan tried to make home buying more affordable by stretching loan terms. They offered 100-year mortgage terms, but it didn’t have the desired effect.

The idea behind a 100-year mortgage was that the home and debt could be passed down through the generations, kind of like generational wealth.

But it didn’t really make home buying more affordable for regular folks. Instead, affluent homeowners were more likely to get these long-term mortgages as an estate-planning tool to reduce inheritance taxes.

So what can first-time home buyers do?

If you’re a first-time home buyer, look into down payment assistance programs.

For example, Michigan is offering a First-Generation Down Payment Assistance Program, which will provide qualifying first-time buyers with up to $25,000 to help cover a down payment, closing costs and prepaid escrows. At the time of writing, the program’s available funds have been committed, but programs like this exist.

Focus on saving a down payment to reduce your monthly payment instead of stretching out your loan. It’ll just mean paying more interest in the long run and taking years to own a chunk of your home.

Bottom line

Longer mortgages won’t fix the root issue of homes being unaffordable — there’s a limited supply of homes to begin with, and a 50-year mortgage can mean paying double the interest.

These homeowners would be locked into a mortgage and unable to refinance for nearly 40 years unless they can put down a significant down payment.

This story was produced by Finder.com and reviewed and distributed by Stacker.