New report projects 22% increase in car insurance costs after 15% spike in first half of 2024

This story was produced by Insurify and reviewed and distributed by Stacker.

New report projects 22% increase in car insurance costs after 15% spike in first half of 2024

Car insurance rates have soared in post-COVID-19 years, and despite many insurance industry experts predicting slower rate hikes in 2024, data from the first half of the year shows a 15% increase in full-coverage premiums. Insurify's data science team projects a total 22% increase in 2024.

Rate increases in 2024 are largely a continuation of hikes in 2023, a year that saw full-coverage premiums rise by 24% in response to insurers' record underwriting losses ($33.1 billion) in the year prior. Underwriting losses decreased to $17 billion in 2023—a financial hit that was still substantial enough to drive significant rate hikes in the first half of 2024.

Insurer losses result from a combination of inflationary pressures—like the rising cost of vehicle repairs and the skyrocketing price of new cars—and unprecedented climate catastrophes that drive weather-related claims in states that haven't historically seen as much of this type of damage. These costs strain insurers' budgets as they pay out more than they earn in profit.

Additionally, legislative changes in states like South Carolina and Maryland have increased insurers' financial responsibility, leading them to charge higher premiums. In California, which froze insurance rates during the COVID-19 pandemic, some insurers are requesting double-digit hikes as they struggle to return to profitability, while others are exiting the state entirely.

Insurify's data science team analyzed average car insurance rates across the United States to determine where drivers saw the most significant increases and which factors pushed up premiums in the first half of 2024.

Key Takeaways

- The cost of full-coverage car insurance increased by 15% in the first half of the year, despite industry expert predictions that rate hikes could slow in 2024. The average annual full-coverage premium now costs $2,329, according to Insurify data.

- Insurify predicts California, Missouri, and Minnesota could see car insurance costs increase by more than 50% in 2024. Damage from severe storms and wildfires contributes to rising rates in the states.

- Maryland has the highest car insurance costs in the U.S., with an average full-coverage rate of $3,400 annually. New Hampshire drivers pay the least, at an average of $1,000 annually.

- Vehicle maintenance and repair costs have increased by nearly 38% over the past five years, according to the Bureau of Labor Statistics Consumer Price Index. Higher repair costs mean insurers pay more expensive claims and policyholders see higher premium hikes.

- Increasingly severe and frequent weather events are driving up auto insurance premiums. Hail-related auto claims represented 11.8% of all comprehensive claims in 2023, up from 9% in 2020, according to CCC Intelligent Solutions.

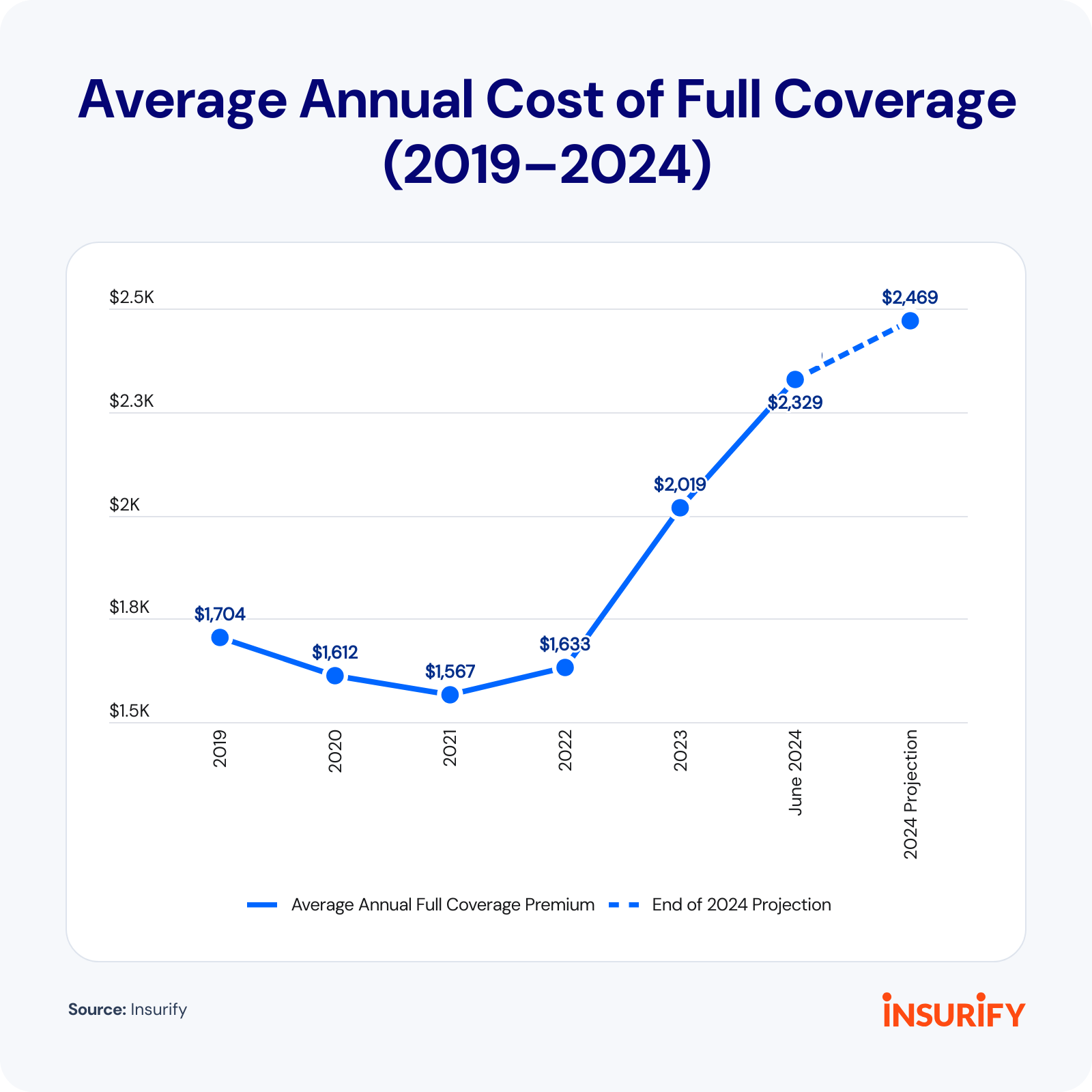

Car Insurance Costs Surpassed $2,300 in the First Half of 2024

The average annual cost of full coverage hit $2,329 in June 2024, a 15% increase from $2,018 at the end of 2023. Drivers could see a total increase of 22% in 2024, with average premiums of $2,469 by the end of the year, according to Insurify's data scientists.

A full-coverage policy includes comprehensive and collision coverage in addition to liability coverage. While most states require liability coverage, comprehensive and collision coverage are optional but provide drivers with greater financial protection for their own vehicles.

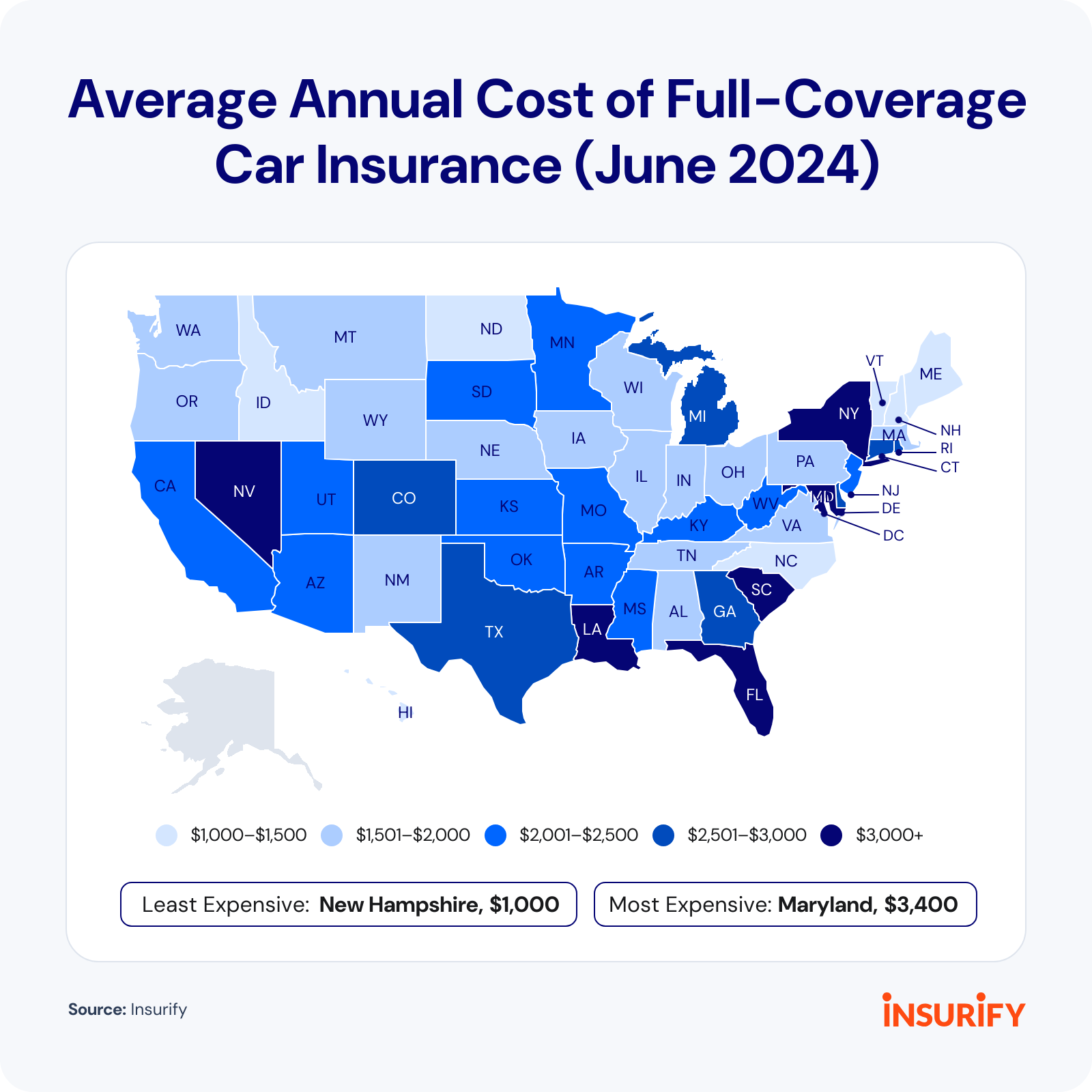

Each state has its own insurance regulations and risk factors, so premiums vary across the U.S. The average annual cost of full coverage is more than $3,000 in six states: Florida, Louisiana, Maryland, Nevada, New York, and South Carolina. New Hampshire drivers pay the least, at an average annual rate of $1,000.

The 10 Most Expensive States for Car Insurance

Some states with the most expensive full coverage in the U.S., including Maryland and South Carolina, saw legislative changes over the past year that increased insurers' financial responsibility. These changes could contribute to higher premiums as insurers re-evaluate their rates to meet higher coverage expectations.

Key Factors Behind High Car Insurance Rates in Top States

Three of the 10 most expensive states for car insurance—Florida, Michigan, and New York—have no-fault systems. In these states, drivers file claims with their own insurance companies to receive compensation for their injuries, no matter which party caused the accident. No-fault systems are supposed to speed up claims but have also provided opportunities for insurance fraud.

Other states with sky-high insurance rates, like Florida, Louisiana, and Nevada, face weather-related damages from hurricanes and wildfires. While climate risk has historically affected homeowners insurance more than auto insurance, insurers factor in the risk of car damage from hail, wind, and falling objects.

Vehicle theft rates, traffic congestion from high population density, and an increase in car accidents also contribute to higher rates. Insurify analyzed the 10 most expensive states for car insurance to identify the hidden factors affecting policyholders.

1. Maryland

- Average annual cost of full coverage: $3,400

- Percent higher than the U.S. average: 46%

- Projected average rate increase in 2024: 41%

Maryland drivers pay the most for full-coverage car insurance, with an average monthly cost of about $283. The state's 43% year-over-year rate increase may be partially explained by a spike in traffic fatalities. Maryland saw an 8.2% rise in motor vehicle crash deaths in 2023, while on average the U.S. saw a 3.6% decline, according to the National Highway Traffic Safety Administration, or NHTSA.

New Maryland legislation, effective July 1, 2024, requires auto insurers to provide enhanced uninsured motorist coverage. The provision allows policyholders to "stack" the at-fault driver's liability insurance with their personal uninsured or underinsured motorist (UM/UIM) coverage. Insurers account for this increased financial responsibility when setting rates.

2. South Carolina

- Average annual cost of full coverage: $3,336

- Percent higher than the U.S. average: 43%

- Projected average rate increase in 2024: 38%

Full-coverage rates in South Carolina soared 43% year-over-year to $278 per month as of June 2024. South Carolina ranks 13th in the U.S. for questionable vehicle-related insurance claims, according to the National Insurance Crime Bureau, or NICB.

Insurers consider fraud risk when setting rates. Weather-related damages from an active 2024 hurricane season are also a risk insurers have to price in.

A 2023 South Carolina Supreme Court decision increased financial responsibility for insurance companies, ruling that auto insurers can't limit property damage claims to just covered vehicles under UM/UIM coverage. Under the new law, insurers have to effectively cover all properties registered to the policyholder and their family.

3. New York

- Average annual cost of full coverage: $3,325

- Percent higher than the U.S. average: 43%

- Projected average rate increase in 2024: 4%

New York drivers previously had the most expensive full coverage in the country at the end of 2023 but saw a 1% decrease in the first half of 2024 as rates in other states skyrocketed. New York is the ninth most densely populated state in the U.S., which contributes to higher insurance costs due to the greater risk of claims.

New York also has the highest number of stolen cars in the U.S., with 32,715 thefts in 2023, NICB data shows. The higher likelihood of vehicle theft increases the risk of an insurer having to pay out a claim, leading to higher premiums in New York.

4. Nevada

- Average annual cost of full coverage: $3,271

- Percent higher than the U.S. average: 40%

- Projected average rate increase in 2024: 20%

Nevada drivers have seen a 20% increase in full-coverage premiums since June 2023, bringing the average monthly cost to about $273. The state had the third-highest vehicle theft rate in 2023, with 572.7 car thefts per 100,000 residents, according to the NICB, increasing the financial risk of insuring Nevada drivers.

Nevada's rising climate risk could play a large role in future rate setting. Wildfires burn an average of 450,000 acres in Nevada annually, and the state also sees some damage from hurricanes and tropical storms. These weather events increase the likelihood of fire and flood damage to cars in the state and drive up insurance premiums.

5. Florida

- Average annual cost of full coverage: $3,201

- Percent higher than the U.S. average: 37%

- Projected average rate increase in 2024: 18%

Florida drivers pay about $267 monthly for full coverage. The state's ongoing insurance crisis, influenced by severe weather events, has pushed some insurers out of the state entirely, while others have declared insolvency. In 2023, Farmers Insurance stopped offering coverage in Florida, and AAA non-renewed certain home and auto insurance policies.

Over the past two years, Florida has seen a flurry of legislative activity aimed at reducing frivolous lawsuits against insurers, lowering consumers' insurance rates, and mitigating auto insurance fraud. The no-fault state accounts for 74% of questionable auto glass claims in the U.S., according to the NICB.

Despite attempts to reform the state's insurance regulations, Florida remains a difficult state for insurers to profit in—and, as a result, it has one of the country's highest average auto insurance rates.

6. Louisiana

- Average annual cost of full coverage: $3,182

- Percent higher than the U.S. average: 37%

- Projected average rate increase in 2024: 23%

Louisiana drivers pay an average of $261 monthly for full coverage. The state's growing insurance crisis, tied to Louisiana's high hurricane and tornado risks, has mostly affected home insurance. However, the state's climate risk is also beginning to impact car insurance rates, as comprehensive coverage—one part of a full-coverage policy—protects against damages sustained in a weather event.

Louisiana also saw a 10% surge in vehicle thefts in 2023, according to NICB data. Both factors increase insurer risk and, therefore, car insurance rates.

Louisiana lawmakers passed a series of auto insurance reforms in 2024. The laws target excessive medical billing in personal injury lawsuits and limit policyholders' time to file an immovable property claim to two years after the policyholder knows (or should know) about the damage. These reforms, aimed at lowering rates, reduce some insurer responsibility.

7. Delaware

- Average annual cost of full coverage: $2,982

- Percent higher than the U.S. average: 28%

- Projected average rate increase in 2024: 13%

Delaware drivers pay about $249 monthly for full coverage, a 9% increase since June 2023. The state has the seventh-highest population density in the country, according to Census Bureau data, which can increase the odds of accidents and claims on busy roadways.

In one bright spot for policyholders, the Delaware Department of Insurance adopted a new regulation in January 2024 requiring insurers to promptly refund any unearned auto insurance premiums (meaning payment for the unused days of coverage after a driver cancels their policy).

8. Washington, D.C.

- Average annual cost of full coverage: $2,977

- Percent higher than the U.S. average: 28%

- Projected average rate increase in 2024: 17%

Drivers in the District of Columbia saw a 17% year-over-year increase in full-coverage rates, bringing the average monthly cost to $248.

Washington, D.C., has the highest population density in the nation. The district also saw traffic fatalities increase by more than 40% between 2022 and 2023, according to NHTSA data. This combination of factors raises the probability of an insurer having to pay out a claim, so companies increase the price of car insurance in response.

Premium increases may soon slow in D.C. The D.C. legislature passed a new law requiring home and auto insurers to file for prior approval to raise rates. Excessive hikes require notice and an opportunity for a hearing. Previously, D.C. had a file-and-use system, meaning insurers could raise rates immediately after filing with the Department of Insurance.

9. Michigan

- Average annual cost of full coverage: $2,719

- Percent higher than the U.S. average: 17%

- Projected average rate increase in 2024: 8%

Michigan adopted a no-fault insurance system in 2019 in an attempt to lessen rate increases. The state saw a 4% increase in full-coverage premiums between June 2023 and June 2024, compared to a 28% rise nationwide, but Michigan still has some of the highest rates in the country, at an average of nearly $227 per month.

The Michigan Department of Insurance and Financial Services Fraud Investigation Unit received 3,789 fraud reports between July 1, 2023, and June 30, 2024. Of those reports, 99% were insurance-related, and 50% involved auto and no-fault claims. Higher fraud rates make the state riskier for insurers to operate in, and they raise rates in response.

10. Georgia

- Average annual cost of full coverage: $2,688

- Percent higher than the U.S. average: 15%

- Projected average rate increase in 2024: 24%

Georgia drivers pay an average of $224 monthly for full coverage. Vehicle thefts might influence the state's high car insurance costs since insurers factor that risk into rate setting. Georgia drivers reported 28,171 cars as stolen in 2023, the ninth-highest number in the nation, according to NICB data.

On July 1, 2023, House Bill 221 went into effect, ending the state's file-and-use provision and giving Georgia's insurance commissioner 60 days to review rate filings before insurers can implement increases. Despite the new legislation, Georgia drivers saw a 21% increase in full-coverage costs between June 2023 and June 2024.

States Where Car Insurance Is Rising Fastest in 2024

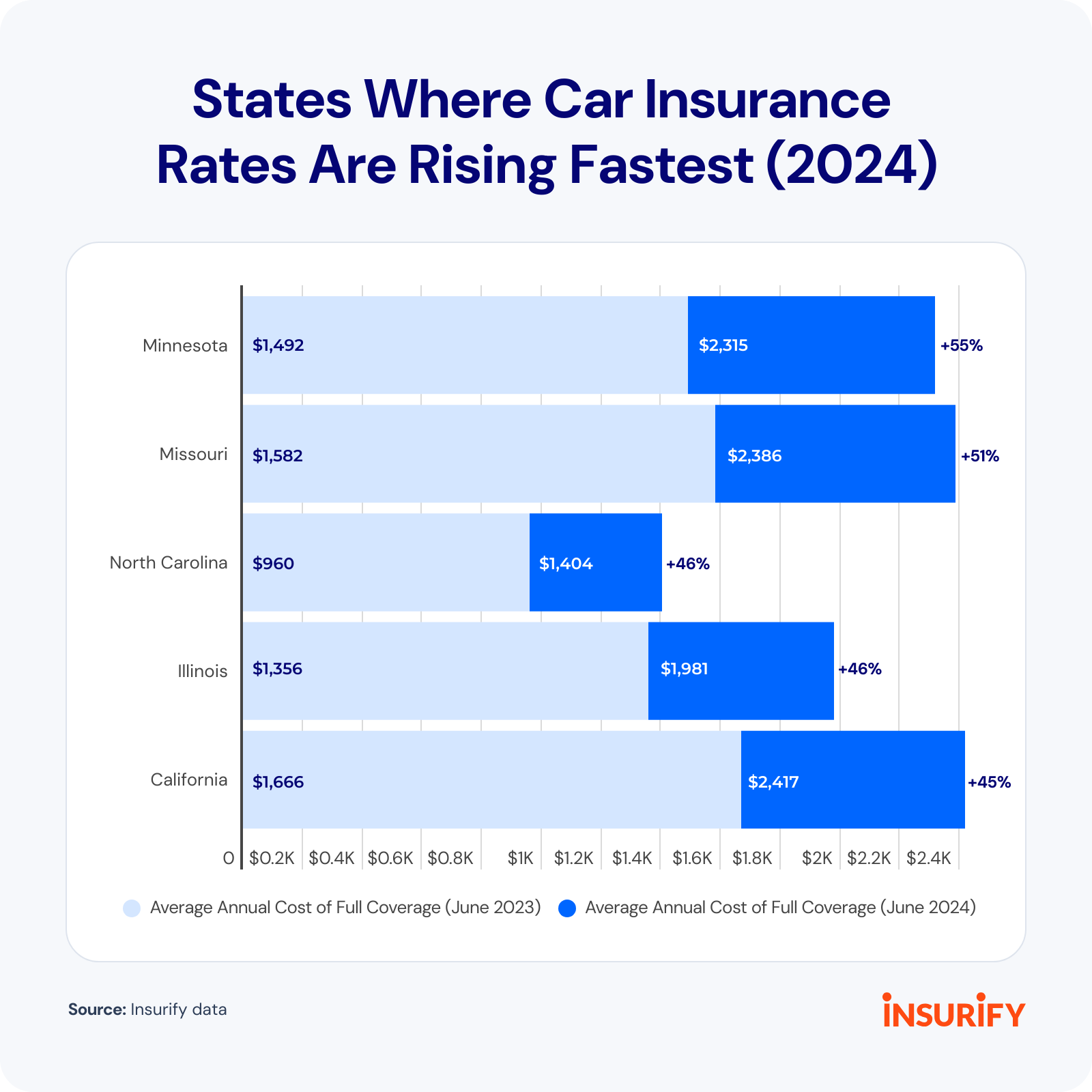

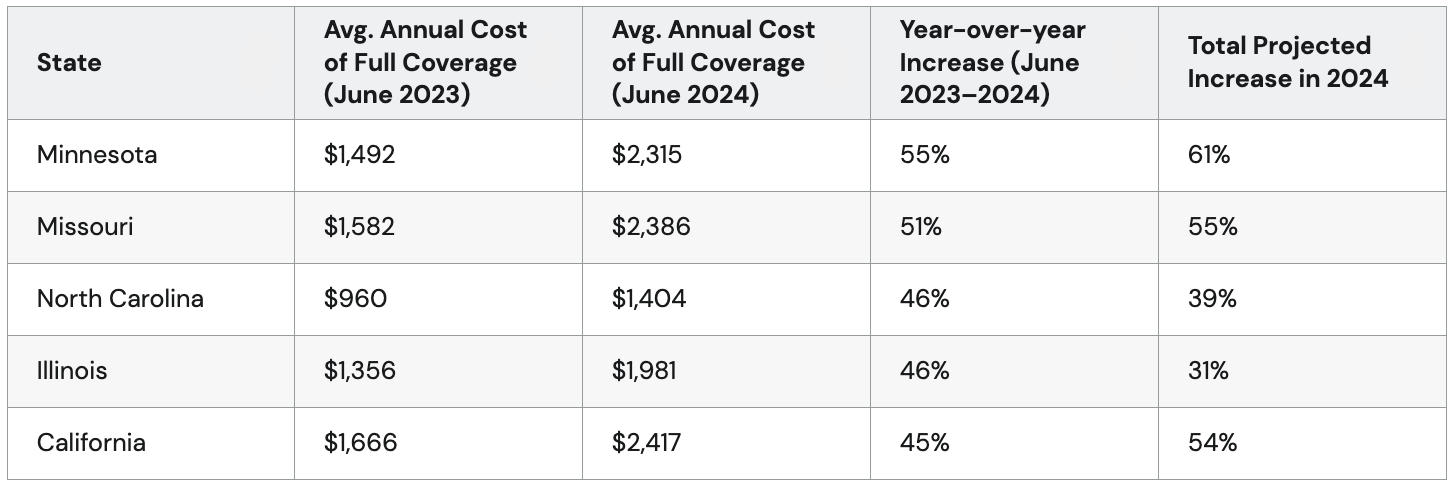

The cost of full coverage across the U.S. increased by 28% between June 2023 and June 2024—but drivers in some states are seeing year-over-year rate hikes of more than 50%.

The reasons behind these extreme increases vary and compound. From hail to hurricanes, shifting weather patterns due to climate change are driving up claims and, consequently, premiums in some states. Others are seeing higher rates of car thefts or the effects of legislative changes.

Severe Weather and Rising Theft Rates Drive Up Auto Insurance Costs

Minnesota, which saw a 55% increase in rates, experienced a total of $1.8 billion in damage following a series of storms that dropped golf-ball-to-baseball-sized hail across the Twin Cities in August 2023.

Severe convective storms also hit Missouri and northwest Illinois in 2023. A supercell produced golf-ball-sized hail and heavy rains, forming a tornado along its track as it moved across the states.

North Carolina faces a different weather risk—hurricanes. In 2023, Hurricane Idalia hit the state. While the hurricane weakened to a tropical storm, it still brought damaging high winds, heavy rainfall, and local flash flooding to the state. Storms like this cause water damage to cars, which insurers pick up the cost of if drivers have comprehensive coverage.

Car thefts drive up premiums, too. Missouri and California are among the 10 states with the highest auto theft rates per capita, and Illinois had the fifth-highest number of stolen cars in 2023, NICB data shows.

California Is Now Playing Catch-Up

California's insurance regulations emphasize consumer protections, requiring approval from the Department of Insurance, or DOI, before insurers can implement rate increases. Drivers in the state still saw a 45% year-over-year full-coverage rate increase in the last year.

"During COVID-19 shutdowns, states like California put a freeze on rate increases. That's why so many people saw drastic rate hikes in 2023 after those restrictions were lifted," said Mallory Mooney, a licensed insurance agent and director of sales and service at Insurify. "Insurers are still playing catch-up, and it's too little too late for a lot of them. Insurers have had to pull out of some markets completely."

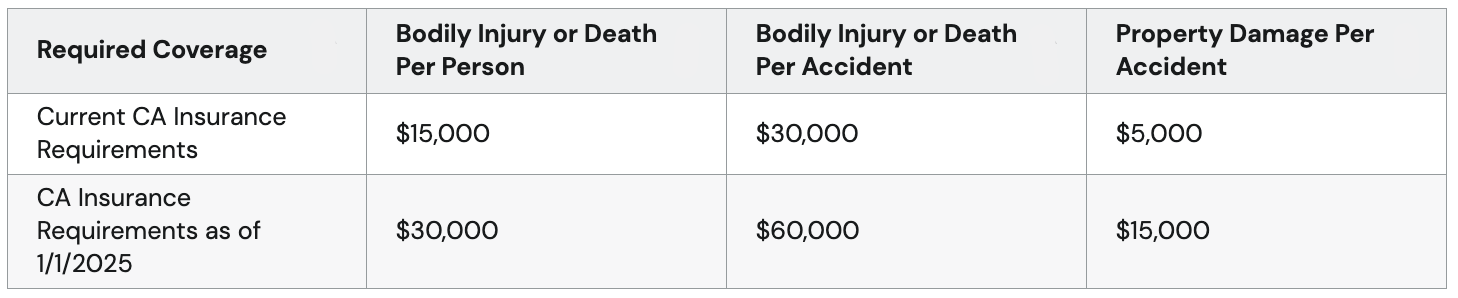

Additionally, California is increasing its minimum car insurance requirements to bring them in line with other states. California governor Gavin Newsom signed Senate Bill 1107 into law in late 2022, doubling and, in some cases, tripling the liability limits for auto insurance policies. The change goes into effect Jan. 1, 2025.

This means California residents will see even higher premiums next year, albeit with higher protection limits as well. The higher limits will prevent more drivers from going into debt after a car accident, but since it increases the financial burden on insurers, they will raise rates to match the new requirements.

Insurers Face Challenges in California's Strict Market

California's consumer protection laws keep insurance costs down for policyholders, but it's difficult for insurers to operate profitably. The state's DOI is slow to approve rate hikes, and insurers have pulled back on writing policies. GEICO has closed all its California offices, State Farm has stopped quoting via phone, and Progressive has halted advertising in the state.

As more insurers leave the state, the DOI may approve additional rate increases to keep companies in the market.

Climate Change Plays a Growing Role in Auto Insurance Rate Setting

Climate risk has historically affected homeowners more than auto insurance—but growing damages from weather events, which comprehensive car insurance often covers, are changing how insurers set rates.

"I think climate risk will likely start to play a role in new areas. As we experience tornadoes, hail, and flooding in places where they weren't necessarily a major threat before, the increased frequency and severity of these events will need to be considered in pricing," said Betsy Stella, vice president of carrier management and operations at Insurify.

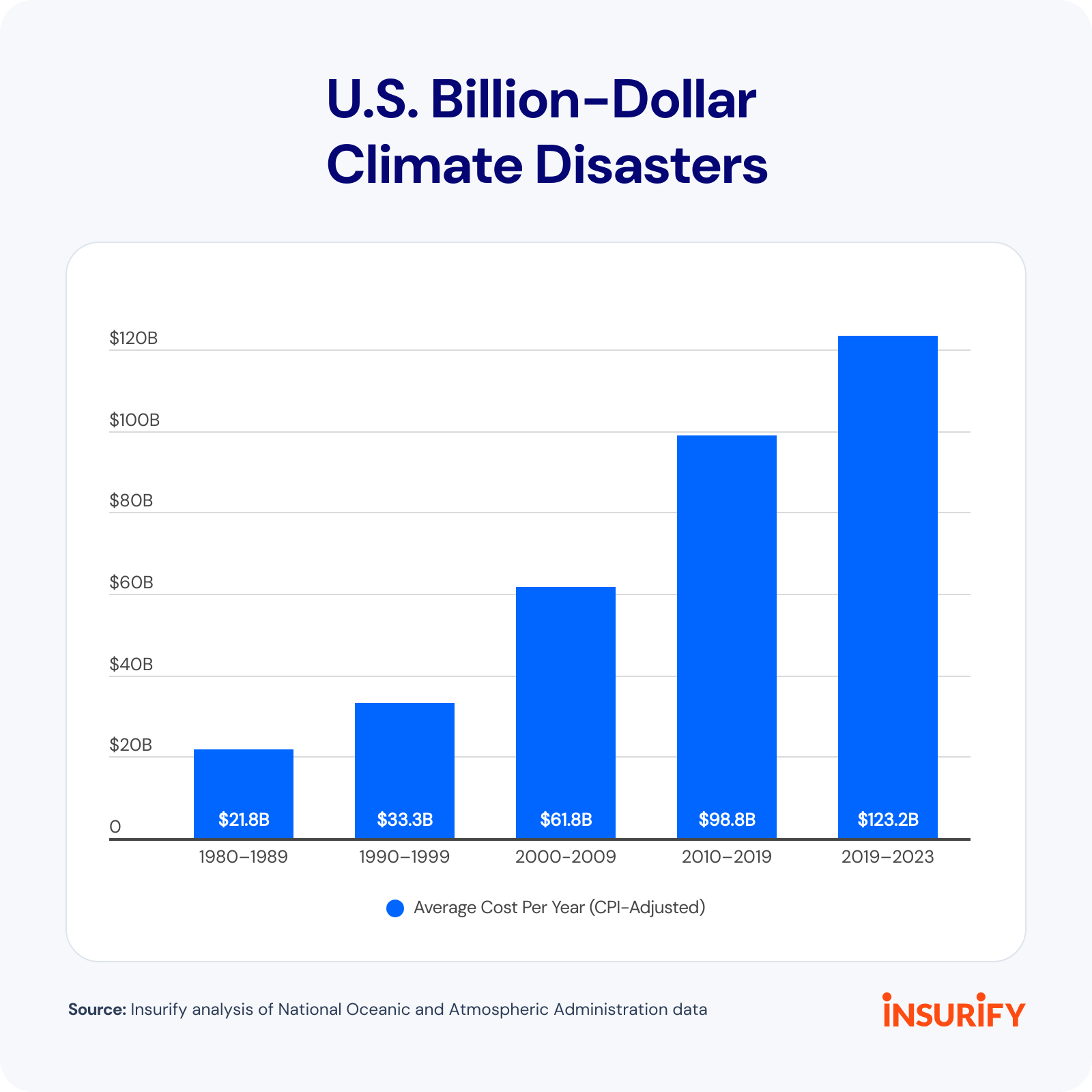

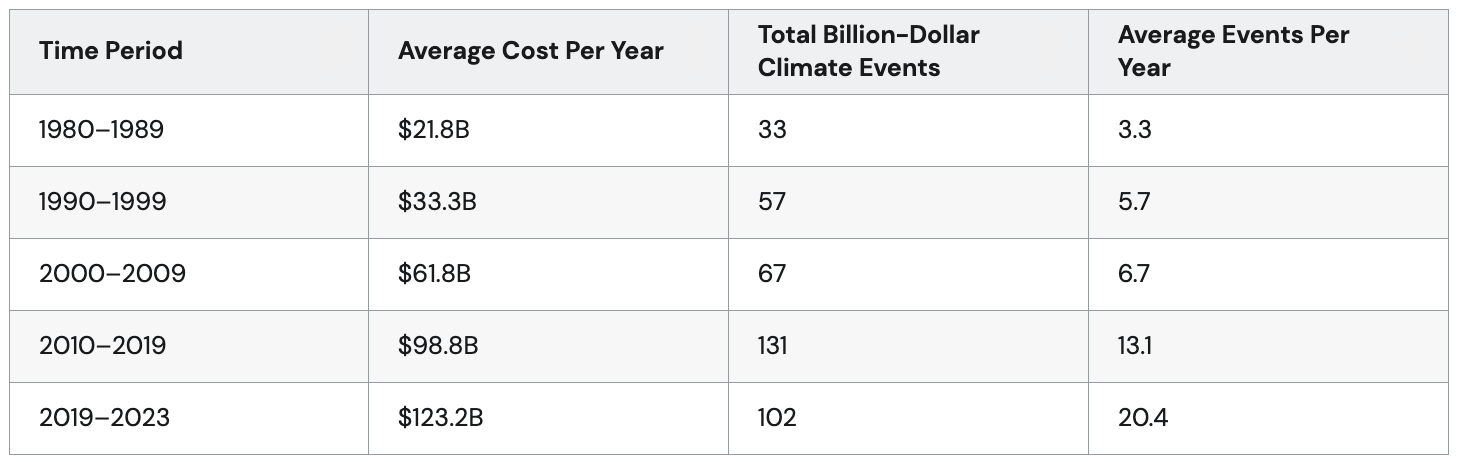

Climate events that cause $1 billion or more in damage are increasing. The U.S. saw an average of 20.4 billion-dollar weather events per year between 2019 and 2023—a 56% increase from an average of 13.1 events annually between 2010 and 2019, National Oceanic and Atmospheric Administration (NOAA) data shows.

Rising Weather-Related Claims Drive Up Auto Insurance Premiums

During Hurricane Ian's peak days, Sept. 25–30, 2022, nearly 52% of Georgia, Florida, and South Carolina vehicle claims were total losses, according to CCC Intelligent Solutions.

Severe thunderstorms cause less damage as single events but accounted for 70% of all insured natural catastrophe losses in the first half of 2023, causing $34 billion in losses, Swiss Re data shows.

Hailstorms are particularly destructive. Auto losses from a single hailstorm could exceed $130 million, with each claim costing around $5,000, according to CCC estimates. Eighty percent of auto insurance hail claims require paintless dent repair (PDR)—a fix that costs 28% more than non-PDR claims.

Insurers raise premiums to cover more expensive weather-related claims, but they're also paying for reinsurance—essentially insurance for insurers. Reinsurance companies spread out the cost of catastrophic losses and raise insurers' rates in response to increasingly severe and frequent climate events.

"Consumers can expect to see increased reinsurance costs passed along to them," said Stella.

Drivers in hurricane-prone areas may be especially likely to see rising reinsurance rates affect their premiums. The NOAA predicts the U.S. will see above-normal levels of Atlantic hurricane activity in the summer and fall of 2024.

Newer Cars With More Expensive Repairs Put Upward Pressure on Insurance Rates

New vehicles often have thousands of fragile semiconductor chips to support advanced features like collision, lane-departure, and blind-spot warnings. Safety technologies can help drivers avoid crashes and accident-related premium hikes but are also expensive to repair.

Vehicle maintenance and repair costs have increased by nearly 38% over the past five years, according to the BLS CPI.

Advanced driver-assistance systems, or ADAS, can add up to 37.6% to the total repair cost after an accident, AAA data shows. Minor damages to front radar and distance sensors can add up to $1,540 to the bill.

EVs pose an additional challenge. They take an average of 5.8 days longer and cost 46.9% more to repair than gas-powered cars, with an average repair cost of $6,700, according to CCC data.

Mechanic labor hours have grown by 40% per claim over the last decade as technologies in newer models become increasingly complex. Finding an auto mechanic without a backlog to perform that labor can be difficult. The U.S. is facing a shortage of 495,000 auto technicians and 110,000 collision repairers, according to a TechForce Foundation study.

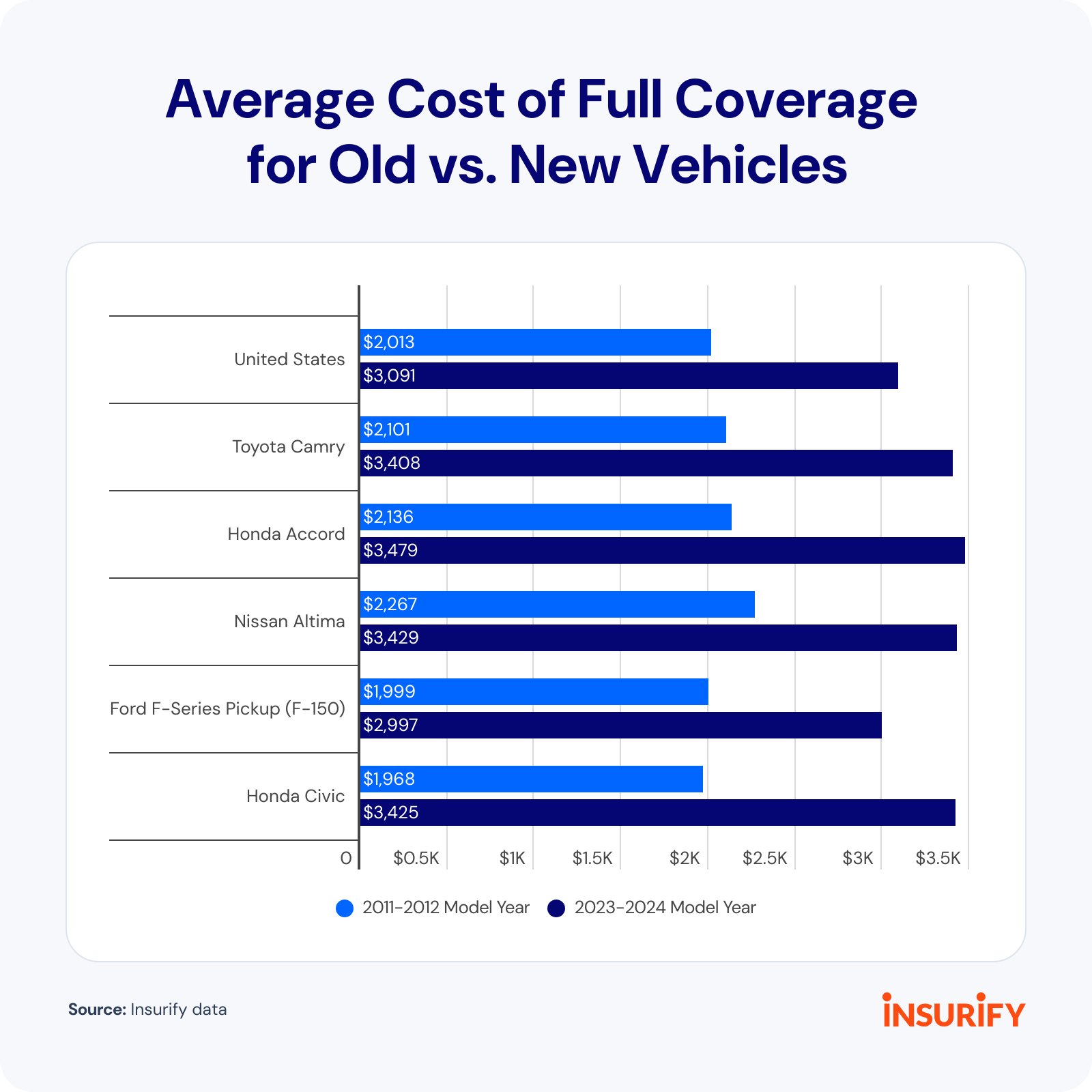

As new vehicle prices have risen and inflation has strained Americans' finances, drivers are holding onto their cars for longer. The average U.S. vehicle age reached a new record of 12.6 years in 2024, according to S&P Global Mobility.

Though most insurers offer new vehicle discounts because the cars are more reliable and safer in accidents, insurance is cheaper for older vehicles. Full coverage for a 2011–2012 model year Honda Civic averages $1,968 annually, but insuring a 2023–2024 model costs 74% more, at $3,425 annually.

The 2024 Honda Civic has multiple high-tech safety features, including lane-keeping assistance, traffic sign recognition, collision mitigation braking, and adaptive cruise control.

Auto Insurers Push Telematics for Relief From Premium Hikes

Drivers facing premium hikes may look to insurance discounts to lower their costs. Most insurers offer numerous ways to save, including bundling home and auto insurance, taking defensive driving courses, and achieving a certain number of years without an at-fault accident or other moving violation.

But insurance companies are increasingly interested in pricing risks based on policyholders' driving behaviors rather than factors like gender, place of residence, or credit-based insurance scores, says Stella. Telematics insurance programs give insurers that ability.

Telematics-based insurance tracks driver behavior through smartphone apps or plug-in devices. Insurers use this driving data to determine premiums, reducing the cost for cautious drivers who follow traffic laws and increasing it for behaviors like hard braking, speeding, and rapid acceleration.

Telematics insurance savings vary. Progressive's Snapshot telematics program saves drivers an average of $231 annually, and Nationwide's SmartRide offers up to 40% off premiums.

"It remains to be seen how much premiums will be reduced for the safest drivers, but there doesn't seem to be doubt [from insurers] that they will be," Stella said. "Insurers also see opportunities to use telematics data to make driving safer for everyone on the road. Alerting riskier drivers to their unsafe behaviors, for instance, may reduce instances of those behaviors—particularly if there are incentives to drive more safely."

Data shows the benefits of telematics for road safety and insurance rates. By participating in a telematics program, the least-safe drivers decreased distracted driving behaviors by an average of 20% and hard braking by 9%, reducing estimated bodily injury claims by 5.5%, according to a Cambridge Mobile Telematics study.

Catastrophic Losses and Expensive Repairs Continue to Strain Insurers and Drivers

Despite signs of market stabilization at the beginning of the year, premium increases have continued in 2024. By the end of the year, Insurify's data science team expects a 22% year-over-year increase in full-coverage rates, bringing the average annual cost to $2,469.

Rising vehicle repair costs and more complicated and expensive fixes for newer cars with ADAS are significant drivers of rising premiums.

Drivers in states with frequent heavy storms, hail, hurricanes, and wildfires—an increasingly large portion of the country—will likely see the effect of climate catastrophes reflected in their premiums. As reinsurance companies raise rates, auto insurers pass some of that cost to policyholders.

But good news may be on the horizon for some drivers.

"Insurers implemented higher rate increases to account for changes in the frequency and severity of auto losses. The COVID-19 pandemic and following inflation, especially in the price of vehicle maintenance and repairs, along with changes in driving behaviors, led to new loss trends that increased the difficulty of rate setting," said Stella.

"Some insurers have started making downward adjustments in areas where they've found opportunities to operate profitably while charging lower rates," she said. "Generally, consumers will continue to see rates rise with inflation, or in areas where traffic accidents are increasing, but in some states, they could see premiums decrease a little again."

In the meantime, drivers who saw their premiums rise can take steps to lower their insurance costs. Comparing rates with multiple insurance companies can help drivers save hundreds of dollars annually on comparable coverage.

Insurers also offer discounts for accident-free drivers, military members and their families, certain vehicle safety features, multi-vehicle policies, and more. Raising deductibles can bring premiums down, and telematics programs can further reduce costs for cautious drivers.

Methodology

Insurify's data scientists examined more than 97 million rates in its proprietary database, quoted via integrations with partnering insurance companies. Driver applications originate from all 50 states and Washington, D.C., and include information on the exact coverage specifications of each driver's quoted policies. Insurify excluded Alaska data due to lower quoting volume.

The premiums in this report reflect the median insurance cost for drivers between the ages of 20 and 70 with clean driving records and average or better credit, unless otherwise noted. Yearly prices in this report are two-year rolling medians to manage extreme market volatility over the past few years.

Liability-only premiums correspond to policies with bodily injury limits between state-minimum requirements and $50,000 per person, $100,000 per accident; property damage coverage between $10,000 and $50,000; and no additional coverage. Full-coverage premiums reflect the same bodily injury and property damage limits, plus comprehensive and collision coverage with deductibles of $1,000. To download more auto insurance data, visit Insurify's data center.