Fourth of July insurance mistakes that could cost you

Planning a road trip or holiday hosting on Independence Day weekend? Many Americans are excited to celebrate the country’s semiquincentennial in just a few weeks. If last year’s travel numbers are repeated — an estimated 72.2 million people journeyed at least 50 miles or more from home over the Fourth of July holiday period in 2025 — we can expect a lot of drivers hitting the highways soon.

But while this July 4 is a surefire cause for celebration, it’s also peak season for insurance claims.

“The Fourth of July creates a perfect storm for insurance claims because several high-risk activities peak at the same time: fireworks use, heavy road travel, grilling, swimming, and crowded gatherings,” explained Janet Ruiz, director of strategic communications for the Insurance Information Institute.

If you’re not careful, even small holiday slipups can lead to injury, car and property damage, and long-term financial consequences in the form of denied claims, premium hikes, and lost discounts — not to mention a lawsuit triggered by a backyard barbecue or swimming mishap.

TheZebra.com took a closer look at common holiday hazards to be aware of and when you should and shouldn’t file a related claim.

The financial fallout of holiday driving

With more drivers hitting the road this time of year, your odds of being involved in a car accident or ticketed for a traffic offense increase significantly. Consider that, between 2020 and 2024, 2,719 people were killed in motor vehicle traffic crashes over the Independence Day holiday period, with 38% of the deceased drivers being intoxicated, per the National Highway Traffic Safety Administration.

If you overindulge on the Fourth and are pulled over for a DUI, expect your car insurance rates to skyrocket. According to The Zebra’s 2026 violation research, the average annual cost for car insurance after a DUI jumps to over $4,400, which is a 98% increase compared to a motorist with a clean record.

“Because these violations stay on your insurance record for three to five years, one mistake can cost you between $10,000 and $15,000 in total extra premiums,” cautioned Beth Swanson, insurance analyst with The Zebra. “And beyond the higher rates, many standard carriers could drop your coverage entirely, forcing you into the high-risk market where costs are even more prohibitive.”

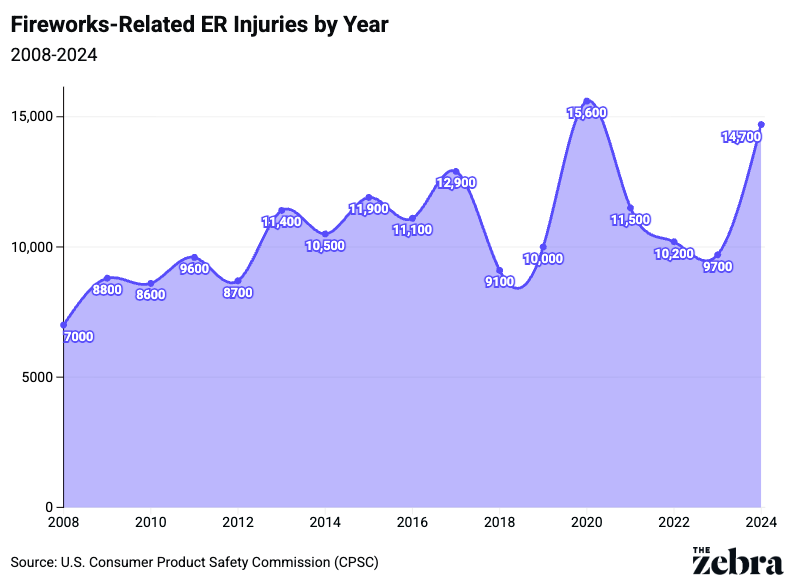

Reap the perks of fireworks safety

Before lighting up those firecrackers, aerial repeaters, Roman candles, and other personal pyrotechnics, think carefully about the fire and injury risks involved. One stray bottle rocket could set your neighbor’s fence ablaze or burn the skin of a bystander. Even if you didn’t light the firework yourself, you are typically on the hook for fires or physical harm that occur on your property or that affect a neighbor’s property.

Swanson notes that a fire-related homeowners insurance claim involving structural damage and smoke now averages over $88,000.

“But what most homeowners don’t realize is that their policy may not cover damage caused by consumer fireworks, many of which are illegal in several states,” personal finance expert Andrew Lokenauth said.

To decrease your liability, create a “wet zone” using a hose and water buckets before you start igniting fireworks. Be sure to clear away dry grass, cardboard, and leaves within 30 feet of your launch area, too.

“Also, keep a fire extinguisher and a first aid kit in a dedicated spot near your grill or back deck,” recommended Swanson.

Practice responsible road-tripping

An early summer road excursion elevates your risk due to longer driving distances, unfamiliar routes, and increased exposure to accidents and vehicle theft.

“The good news is that your personal auto insurance should cover damage to your vehicle, while stolen belongings are typically covered under your homeowners or renters insurance, after you meet your deductible,” Ruiz said.

If you get behind the wheel of an aging car, however, you are increasingly vulnerable.

“Long miles and heavy holiday traffic can also speed up wear and tear on older vehicles,” noted Luke Oswald, automotive specialist with Wheels Away. “Remember that start-and-stop driving adds significant strain on your car’s brakes, cooling systems, and tires.”

That’s why it’s crucial to have your auto checked and serviced before you depart. Insurance doesn't cover wear and tear. It’s also smart to keep your doors locked, place bags and possessions within your car out of sight, and park in well-lit areas near building entrances with security cameras.

Avoid rental car upsells

If you’ll be renting a car this summer, be careful you don’t overpay.

“The rental car counter is one of the biggest upsell environments in travel, and most people walk away paying for coverage they already have,” added Lokenauth. “Before you rent, check your personal auto insurance policy. In most cases, your existing liability, collision, and comprehensive coverage extends to rental vehicles.”

Also, premium credit cards include secondary or even primary rental car coverage when you pay for the rental with that plastic. Primary coverage kicks in before your personal policy does, which means no claim on your record and no hit to your deductible.

“To use this benefit, you must pay for the entire rental with that specific card and decline the rental company’s insurance,” Swanson added.

When you should curb that claim

Insurance comes in handy when you need it most. The problem is, many policyholders file questionable claims they may end up regretting.

“Filing small claims can be costly because the payout may barely exceed — or even fall below — your deductible. Additionally, claims history is a key factor in determining premiums, and even minor claims can lead to higher rates or loss of discounts. In many cases, it can be more economical to pay for minor damages out-of-pocket,” Ruiz suggested.

Swanson seconds those sentiments.“In 2026, insurance companies are more sensitive to claim frequency than ever before,” she said. “If you have a $500 deductible and a firework causes $700 in damage, the insurance company will only pay you $200. That small check could trigger a surcharge that raises your rates by 10% or more for the next three years.”

The bottom line

America's 250th birthday is worth celebrating, just not at the expense of your financial security. Before the cookout starts and the road trip begins, take 15 minutes to pull up your declarations page. Check your liability limits, confirm your rental car coverage, and ask your agent whether your policy covers consumer fireworks damage. A quick call now is a lot cheaper than a denied claim in July.

This story was produced by The Zebra and reviewed and distributed by Stacker.