Most Americans considering personal loans are focused on debt reduction, not spending

Personal loans have become an increasingly common financial tool, offering borrowers flexibility to fund everything from major purchases to unexpected bills. As adoption grows, a key question emerges: What is actually driving interest in personal loans today?

New proprietary data from SoFi suggests the answer may be less about spending and more about financial optimization. As economic pressures continue to shape household budgets, Americans exploring personal loans are largely doing so to regain control of existing debt rather than finance new purchases.

An analysis of 1,350 prospective personal loan borrowers reveals that debt consolidation overwhelmingly drives borrowing, while discretionary or nonessential uses such as travel and large purchases rank far lower. The findings suggest that personal loans are increasingly viewed as structured financial tools for optimization rather than short-term spending solutions.

Below is a closer look at the trends shaping borrower intent.

Methodology: Findings are based on proprietary SoFi data collected from a survey of 1,350 prospective personal loan borrowers conducted Dec. 5, 2025, to Jan. 20, 2026, via a quiz experience on SoFi.com. Percentages reflect respondents’ self-reported answers at the time of participation.

Key Findings

- 57% of prospective borrowers cite debt consolidation as their primary reason for considering a personal loan.

- Nearly 40% say their biggest financial goal is paying off debt faster.

- Almost 90% expect to borrow between $5,000 and $50,000.

- 46% would be first-time personal loan borrowers.

- 51% identify interest rates as their top concern.

- 68% report feeling very confident about managing debt.

- More than 84% describe their income as stable.

Source: SoFi proprietary borrower survey (n=1,350)

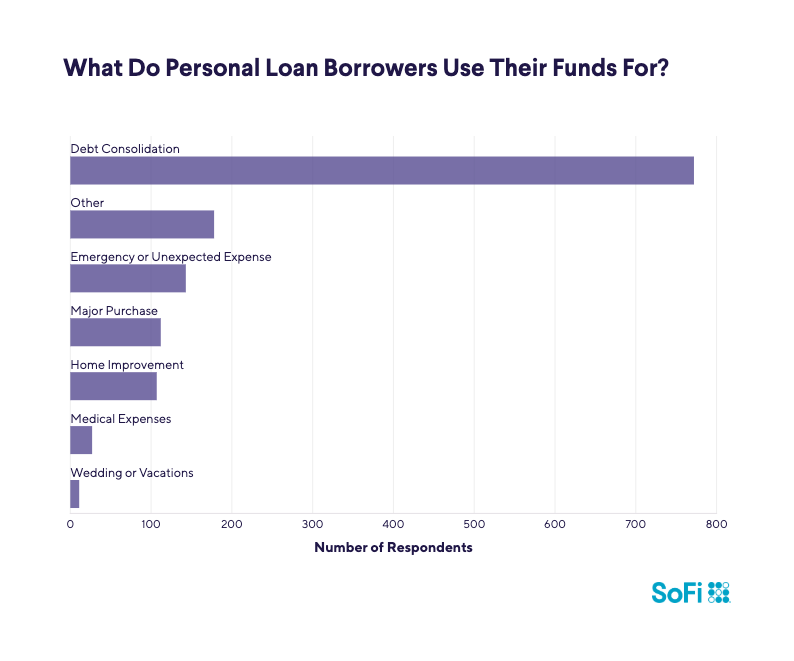

Debt Consolidation Dominates Borrower Motivation

More than half of respondents (57%) report their main reason for considering a personal loan is debt consolidation. That exceeds other motivations by a large margin, including emergency expenses (11%), major purchases (8%), and home improvements (8%).

Debt consolidation involves combining multiple debts into one new loan or credit line, ideally with a lower interest rate, and using it to pay down other debts. Those debts can be credit cards, car loans, or another type of debt. After consolidation, you have just one monthly payment, a fixed interest rate, and a definitive payoff date.

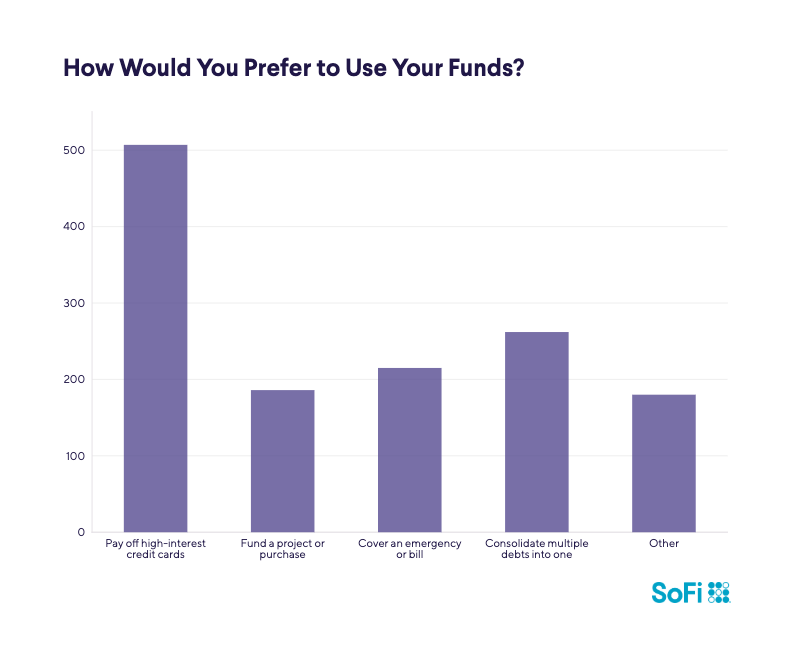

When asked how they would use funds if approved:

- 38% say they would pay off high-interest credit cards.

- 19% would consolidate multiple debts into a single payment.

For example, consider a borrower carrying:

- $10,000 credit card balance at 24.00% APR

- $5,000 on a second credit card at 22.00% APR

- $7,000 auto loan at 8.50% APR

Managing these obligations requires multiple payments, varying interest rates, and separate payoff schedules. In a consolidation scenario, eligible balances are combined into a single personal loan with one fixed rate and a structured repayment term. This replaces multiple payments with one predictable monthly obligation and establishes a clear payoff date.

This example illustrates how borrowers may use personal loans as a financial management strategy focused on restructuring existing debt, rather than financing new discretionary purchases.

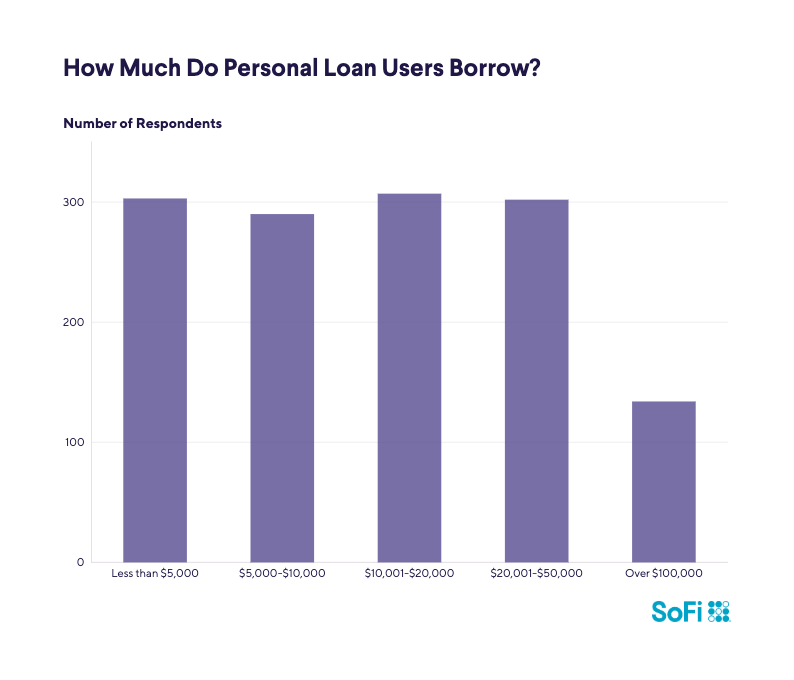

Borrowers Are Targeting Moderate Loan Amounts

Prospective borrowers show relatively even distribution across mid-range loan sizes:

- 22% expect to borrow less than $5,000.

- 21% anticipate $5,000-$10,000.

- 23% estimate $10,001-$20,000.

- 22% project $20,001-$50,000.

- 10% expect to borrow more than $50,000.

Rather than clustering around the highest borrowing ranges, responses are spread fairly evenly across moderate loan amounts, with relatively few respondents expecting to take out larger loans. This distribution suggests borrowers may be sizing loans based on specific financial needs or planned expenses, such as consolidating a defined balance or funding a particular purchase, rather than simply pursuing the maximum loan amount available.

The pattern points to more targeted, purpose-driven borrowing behavior, where loan size reflects a defined objective instead of borrowing capacity alone.

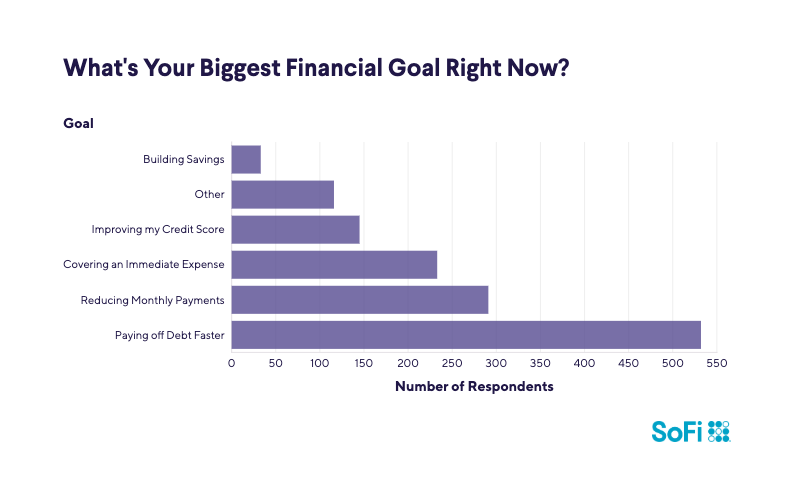

Paying Off Debt Faster Is the Top Financial Priority

With U.S. household debt levels elevated in recent years, public discussion often focuses on consumer borrowing trends and financial resilience. According to the Federal Reserve Bank of New York’s Household Debt and Credit Report, overall household debt balances have continued to grow alongside broader economic changes and shifts in consumer behavior. However, the survey data suggests a more nuanced picture.

Nearly 40% of respondents say their biggest financial goal right now is paying off debt faster, while another 22% aim to reduce their monthly payments. In contrast, fewer respondents prioritize building savings (2%) or improving their credit score (11%), highlighting a strong focus on actively managing existing obligations.

Rather than signaling avoidance or distress, these priorities suggest that many borrowers are taking a proactive approach to debt management. As credit cards, loans, and financing become more integrated into everyday financial planning, debt increasingly functions as a tool that consumers seek to optimize, restructure, and repay strategically as part of broader long-term financial goals.

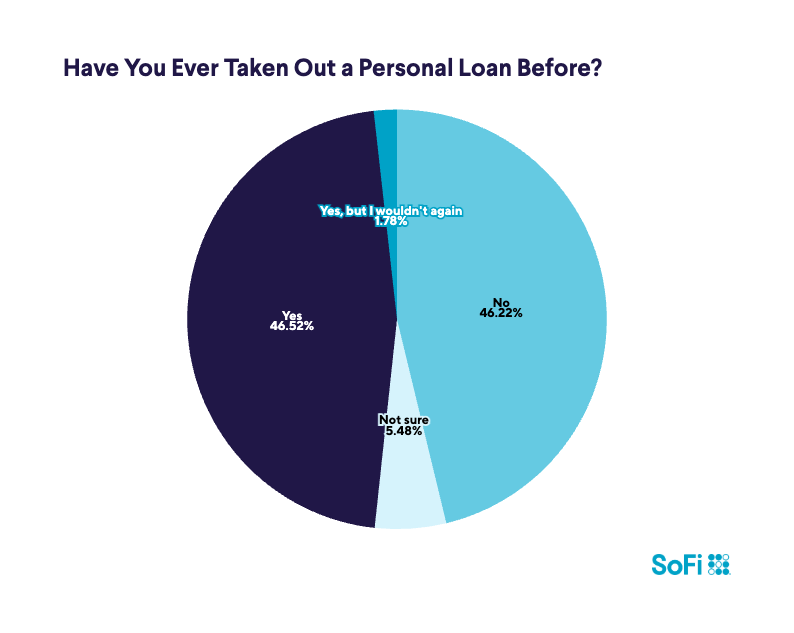

Nearly Half of Borrowers Are New to Personal Loans

Forty-six percent of respondents say they have never taken out a personal loan before, while 47% report having used one previously and finding it helpful.

This near-even split reflects both ongoing adoption among new borrowers and continued engagement from returning users. A substantial share of first-time borrowers suggests the category is expanding beyond traditional audiences, while the strong representation of repeat users indicates positive prior experiences that reinforce ongoing usage. Together, these patterns point to growing familiarity with personal loans as a financial tool, supported by both new entrants and experienced borrowers.

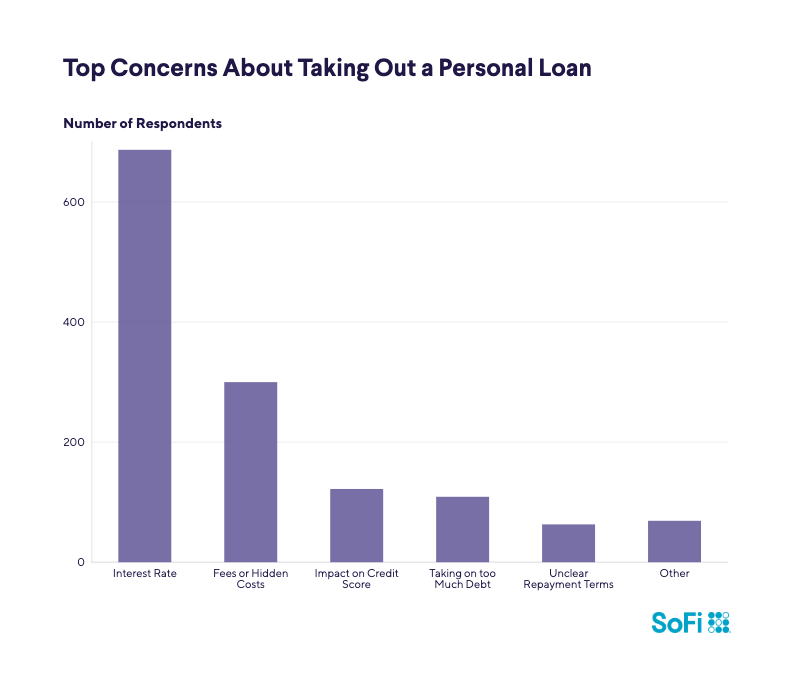

Interest Rates Remain the Biggest Barrier

While personal loans show strong consumer appeal, borrowers remain cautious. A majority (51%) identify interest rates as their primary concern when considering a personal loan.

Other concerns include:

- Fees and hidden costs (22%)

- Credit score impact (9%)

- Taking on too much debt (8%)

Although many Americans perceive current borrowing costs as high, interest rate levels today are closer to longer-term historical ranges compared with the unusually low rate environment seen during the pandemic period, according to Federal Reserve historical rate data. As rates have normalized, consumers appear to be adjusting expectations accordingly.

The data suggests borrowers remain highly rate-sensitive and focused on pricing transparency. At the same time, continued engagement with personal loans indicates that many consumers are becoming more comfortable navigating the current rate environment, evaluating loan options carefully rather than avoiding borrowing altogether.

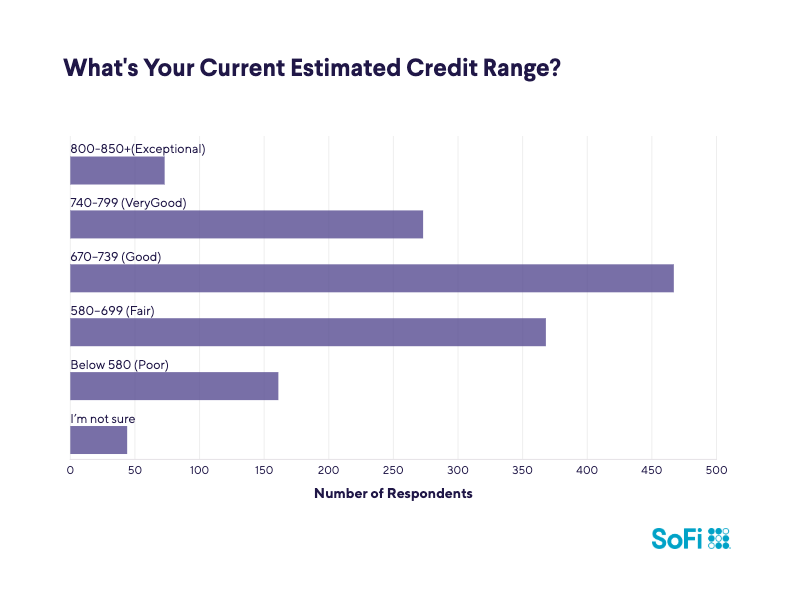

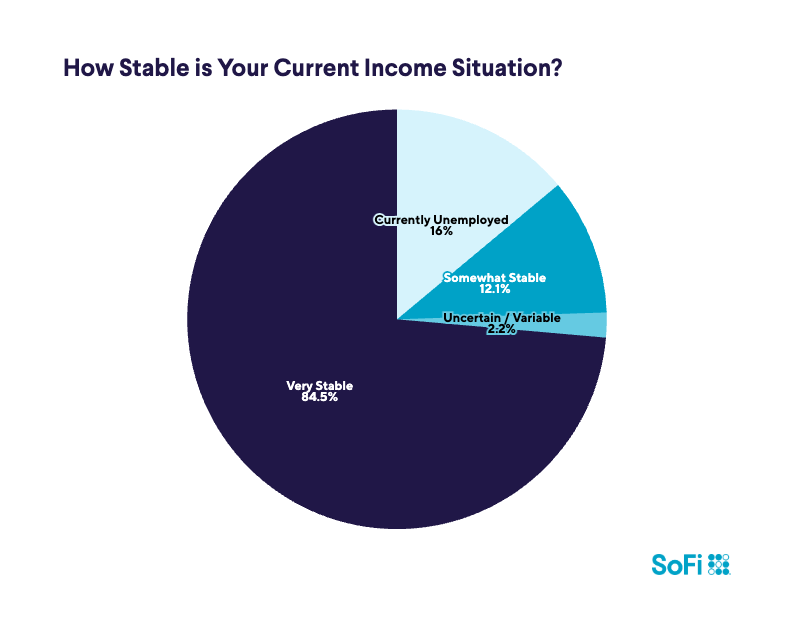

Borrowers Report Strong Financial Confidence and Stability

A notable 68% of respondents say they feel very confident managing debt, while another 26% report feeling somewhat confident, indicating a broad base of financial self-assurance alongside a degree of caution.

Self-reported credit scores cluster primarily in the “good” range (670-739), representing the largest segment at 35%, followed by “fair” (27%) and “very good” (18%).

Additionally, more than 84% of respondents describe their income as very stable.

Financial discussions often distinguish between borrowing used to support longer-term financial goals and borrowing used primarily for ongoing consumption. For example, some consumers use personal loans to consolidate higher-interest balances or restructure payments into a more predictable repayment schedule, while other forms of borrowing may be associated with higher costs or revolving balances. How debt affects a borrower’s financial position depends on individual circumstances and repayment strategy.

Taken together, the high levels of reported confidence, stable income, and generally solid credit profiles suggest that many prospective borrowers are approaching debt as a strategic financial tool rather than reacting solely to financial distress. The presence of both “very confident” and “somewhat confident” respondents also reflects a more measured mindset, where borrowers remain aware of risks while making calculated decisions aligned with their financial priorities.

The Takeaway

SoFi’s internal data highlights a borrower landscape increasingly centered on financial optimization. Rather than using personal loans for discretionary spending, most prospective borrowers appear focused on restructuring and accelerating debt repayment.

While concerns about interest rates persist, the high levels of reported financial confidence and income stability indicate that personal loans are being considered by consumers who view them as strategic tools for improving their long-term financial health.

As household budgets continue to adjust to economic shifts, debt simplification and repayment acceleration may remain dominant drivers of personal loans.

This story was produced by SoFi and reviewed and distributed by Stacker.